Why don’t we hedge more if we want predictable energy bills?

Consumer protection and collateral requirements can get in the way of fixed-price energy bills. Is it the government’s role to intervene?

This is part of a series on UK electricity prices – Part 1: does gas really set electricity prices, Part 2: the benefits of contracts, Part 3: where to cut bills, Part 4: bold energy reforms post-crisis.

When you shop for a mortgage, you can pick a variable rate or fix the rate for up to five years. Usually the interest rate is higher, the longer you lock it in [i]. You choose what you want based on your risk appetite and how much you value predictability. The options for predictable energy bills are more limited, with few providers offering 2-year contracts and none offering longer [ii]. The government sees reducing exposure to “volatile fossil-fuel markets” as part of energy security. If people value predictable bills, then how did British energy customers become so exposed to short-term price swings?

Some energy use is essential, like commuting to work, heating the home in winter or turning the lights on at night, so household energy consumption tends to be ‘inelastic’ to prices. People will pay whatever it takes to meet basic needs. This can mean that during an energy price shock, extra spending on energy eats into discretionary parts of the household budget. It’s also why energy prices rise so much in a physical supply shock, because it takes a dramatic change in costs to drive behaviour to reduce demand.

Because of its importance to voters, energy markets are prone to state intervention. In some countries, governments own their national energy companies, which can reduce the profit-maximising motive to over-charge consumers for energy. In Britain, the energy sector is practically all privatised [iii], which puts us in the global minority for utilities [iv].

The theory in the 1990s was that free markets would bring down energy bills compared to a state-owned enterprise [v]. The government heavily regulated network businesses because as natural monopolies, they wanted to limit investor returns and reduce incentives to overspend on infrastructure. For generators and suppliers, competitive pressure would be enough to keep companies in check.

How price caps impact long-term planning for energy suppliers

But even with competition, private companies were still perceived to be milking their customers, particularly those on default contracts. Savvy customers were offered good deals if they switched suppliers, while the most loyal and passive customers saw prices go up. This dynamic is not unique to energy – it applies to lots of essential products from savings accounts to phone plans [vi].

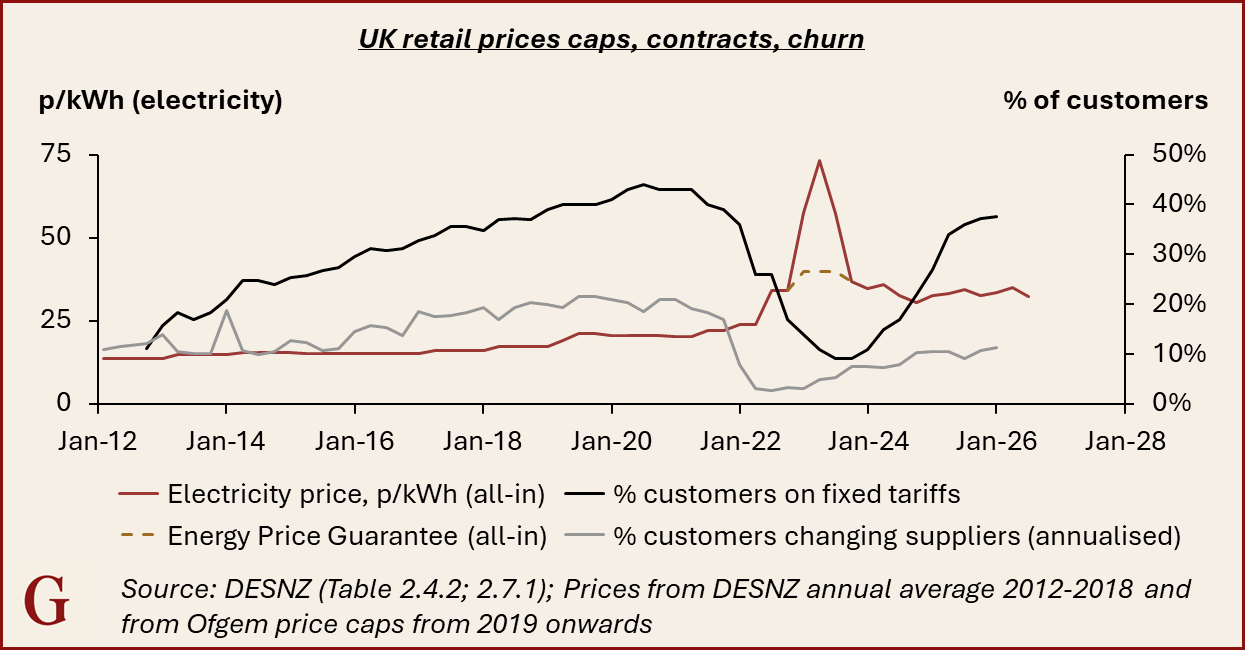

Nonetheless, the government intervened to protect energy consumers after a Competition and Markets Authority review in 2016. They set periodic caps for the price of the default energy bills from 2019 onwards [vii], stopping energy suppliers from over-charging customers who stayed on uncontracted tariffs.

This price cap could be contributing to instability in energy prices. It uses prices that are up to 4.5 months out of date by the time they come into effect [viii]. Under this methodology, the price cap from July to September 2026 will be based on prices observed from February to May. The cap also assumes prices will be smoothed over the following 12 months. Meanwhile, the ~60% of customers who have the default tariff can switch at any time without a penalty [ix]. One in ten households switched suppliers in 2025.

Capping prices solved a problem for disengaged customers but seems to disincentivise long-term planning and stability. Suppliers [x] face asymmetric downside risk when locking in their electricity supply agreements for longer than the three-month price cap period. If prices go up on average, suppliers can always raise prices along with competitors. If prices go down, they risk being locked into costly supply contracts for the customers which stay, and their are on the hook for supply contracts for households they no longer serve if they switch to another provider. The lag between price observation and price changes adds to the difficulty in hedging customer demand. When the Ukraine War broke out, many suppliers were not sufficiently hedged, leading to bankruptcies because their costs became too high for their expected revenues [xi].

Contracts are not attractive at the top of the market but nobody knows exactly when the peak will be. The proportion of customers on fixed tariffs peaked at the dawn of the 2022 energy crisis, at around 40% of UK households. This fell to a low of just 9% in the summer of 2023, suggesting people were unwilling to hedge while prices were high. Switching collapsed around this time as well, as suppliers were bound to charge no more than the cap and could not find ways to make energy any cheaper.

Almost 40% of British households are now on fixed tariffs again. That means 60% of customers [xii] will be exposed to price cap changes if it goes up in response to the Iran War supply shocks, now forecast to increase electricity bills by 11% in July according to Cornwall Insight [xiii]. This is an expensive time to lock in new contracts, but it could get a lot worse.

What about customers who aren’t on default tariffs?

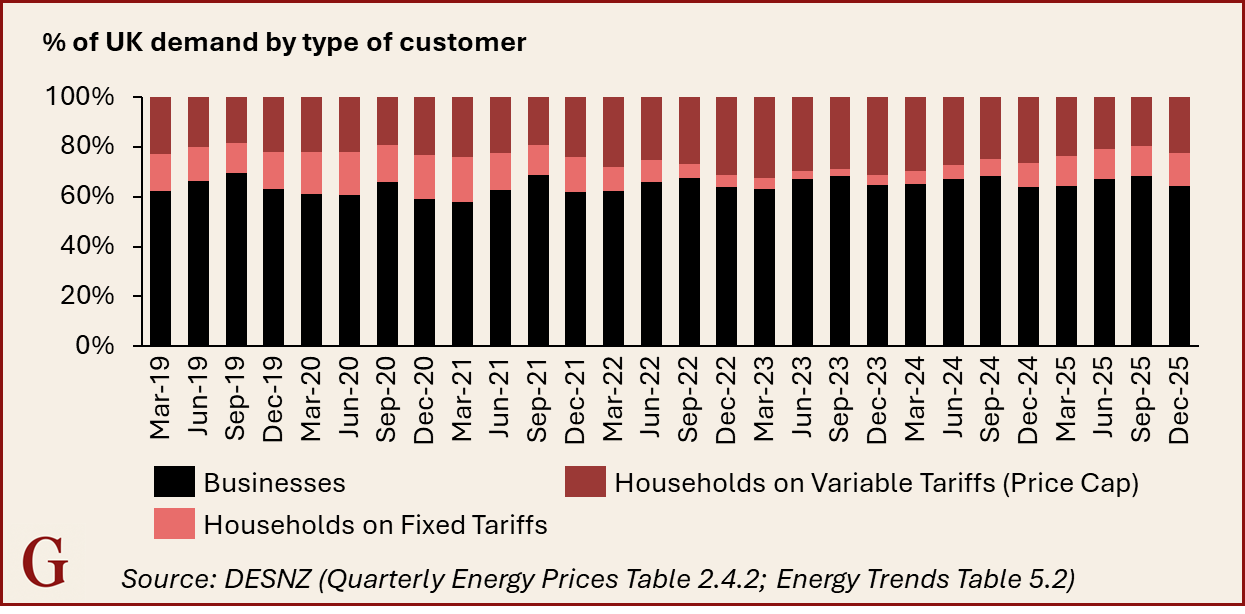

Households are just over a third of final electricity consumption in the UK [xiv]. ~80% of demand across households and businesses is not covered by the price cap [xv], but they are exposed to volatility too.

For households, the costs of switching aren’t particularly high [xvi] even on contracts. Coming back to the mortgage analogy, if interest rates go up, you’re happy you have your fixed contract. If they go down, you can’t switch to a better deal until your contract expires, but at least you agreed to the mortgage based on what you could afford. For energy bills, the same incentives are at play for staying on a good deal as prices rise, but the penalties for ending the contract may not fully reflect the cost for the supplier to get out of their agreements [xvii].

Collateral is another reason why fixed prices aren’t more widely available for longer. When you take out a mortgage, whether fixed or variable, the bank can repossess your house if you aren’t able to pay your bills. For energy, there is no such guarantee for a household, and providing those guarantees as a business is not usually the best use of capital. If the retailer doesn’t match customer contracts with their hedges, they will incur costs to carry that hedge.

While household demand can be predictable year-to-year, businesses may also not have clear line of sight on how their energy demand will shape up. Businesses can procure energy using a power purchase agreement (PPA), but entering into a fixed price contract for a certain amount of volume is a liability if the business closes or energy use declines. Energy generators also typically require credit-worthy counterparties to enter into offtake agreements and smaller businesses are not able to provide this assurance as easily. Hedges also require counterparties willing to bet on the energy price, and beyond a certain timeframe, these prices are difficult to forecast without adding extra costs due to uncertainty.

Does the UK need to ensure long-term, stable prices?

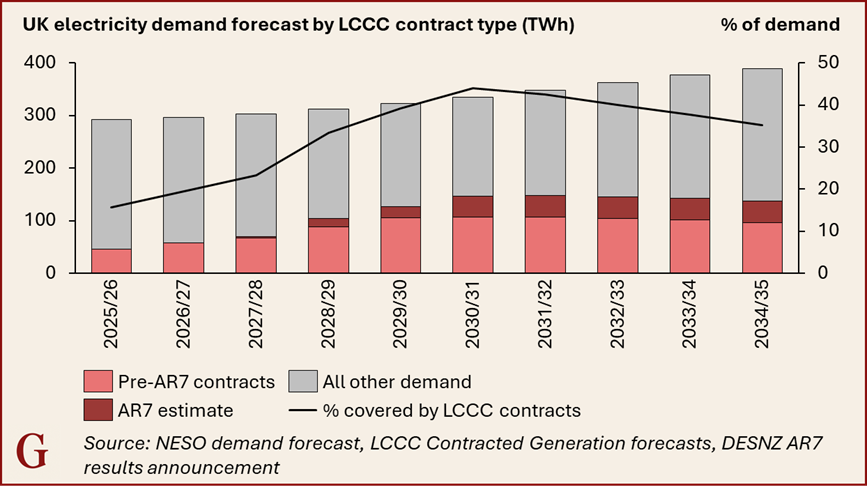

Locking in more of the UK’s energy costs via contracts is an appealing solution for managing price volatility. The government is uniquely placed to do this because of its strength as a counterparty and its ability to agree to pay contracts beyond a few years. The government’s Contract for Difference (CfD) scheme effectively plays this function. Initially conceived as renewable energy support to subsidise and drive down the capital cost of new generation projects, the scheme also serves as a long-term hedge for price stability. 16% of the UK’s electricity generation is covered under the scheme, which could rise to as much as 44% by 2031 [xviii].

The government looks smart if traded power prices go up compared to the CfD contract price, as is happening now with its recently signed offshore wind CfDs [xix], but risks looking like it got a bad deal if prices fall. Either way, the government has bought predictable prices for a share of the energy supply and would expect to pay more than the going wholesale rate for the privilege. This is akin to longer fixed mortgage terms costing more because they price in future uncertainty.

If people value stability, the government could extend contracts to other types of generation, like older renewable facilities or gas [xx]. The government would act as a financial intermediary, absorbing uncertainty that private markets are unwilling to price. It could also sell its hedges back to the market on shorter term horizons to get them off government balance sheets down the line.

The trade-off of government-backed stability is it creates moral hazard and dampens price signals in the short term, which can hinder innovation. If the government is underwriting the cost risk for the long term, there is a lower incentive to be cost-efficient or to pay for one’s own “energy cost insurance”. When more supply is contracted, the cheapest technology for meeting demand in that moment will be unable to compete as effectively to bring down costs, whether it is gas, new renewables, or flexible tech. Contracting in an emergency is also the worst time to sign new deals, but the pressure to do so is lower when the market has recovered from a shock. With the status quo, customers on the price cap struggle when prices go up in a quarter but can benefit immediately when prices come down.

But the price cap was initially designed to protect consumers and is now driving behaviour that exposes them to more volatility. The rest of the market also faces barriers to long-term contracting because financial collateral requirements for fixed prices over long time periods are unaffordable for most customers. The government is the only party which can take on long-dated price risk to provide a form of energy price insurance, and we already socialise other forms of insurance like healthcare. The cost is an energy system that is less responsive to short-term price signals, but this may be worth it to avoid the next cost-of-living crisis outside of anyone’s control.

Enjoyed this piece? Join ~900 followers in 48 countries and subscribe to my Substack for regular long-reads on the energy transition. Share with your friends and colleagues and leave a comment with your thoughts.

Join me at upcoming events

9th April at 6pm: UK Young Energy Professionals Forum Webinar - Energy Across Borders: how the UK and Colombia shape global energy stories. I’ll be a panelist along with Gerard Reid and Ricardo Sierra.

29th April at 9am: Divested interest: Unlocking pension capital for the UK’s clean energy transition – I’ll be a panelist for this event in Shoreditch hosted by Stand. Email me if you’d like to attend.

29th April at 12pm: Innovation Zero 2026 in London: Accelerating the future of cleantech and why diversity matters.

[i] This reflects uncertainty and an insurance-like premium or opportunity cost for the bank. When a downturn is coming or some other trigger of an interest rate drop, the forward curve can invert and signing up to a fixed-rate mortgage for longer can be cheaper.

[ii] Money Super Market comparison website, April 2026.

[iii] The National Electricity System Operator (NESO) is the only state-owned entity in the utility value chain, making decisions on market operations and dispatch. The government owns companies like Great British Energy, and has launched similar state-owned enterprises in the past.

[iv] World Bank Global Power Market Structures database, 2024.

[v] In practice, the UK has ended up with some of the highest electricity costs in the world.

[vi] The UK government is consulting on how to avoid the traps of recurring revenue that tech companies have set, very interested in how this plays out in the UK.

[vii] The initial design was every 6 months, this was changed when the Ukraine War meant that prices were changing too fast to be manageable for suppliers under the price cap.

[viii] The price cap is based on observing 12-month ‘forward’ prices for 3 months, then waiting 1.5 months to apply them. Ben James has a helpful explainer on this here.

[ix] The penalties for customers on contracts aren’t particularly high, either.

[x] Retailers are called ‘suppliers’ in the UK, but they are the last point of supply – suppliers have their own suppliers of energy.

[xi] This was not just due to the price cap design, but it was a factor – the price cap was previously for 6 months, with an ‘observation’ window of 6 months plus a wait period of 2 months before the caps came into effect, leading to a serious lag in price caps versus the real-time market. Firms also were capitalised too thinly to hold hedges, or chose not to for their business model.

[xii] Incidentally, Londoners are less likely to fix their contracts than the rest of the UK (9 percentage points lower than the average proportion of customers on fixed contracts in 2025), which makes this a regional story too.

[xiii] Figures as at 1st April 2026.

[xv] DESNZ Quarterly Prices Table 2.4.2, assuming the share of household customers on fixed prices is applied to demand.

[xvi] Around £50 to £100 based on my scan of Money Super Market.

[xvii] “Breaking” a hedge incurs costs if your hedge is “out of the money”. This happens if prices go down but you have agreed a higher price. If your hedge is “in the money”, i.e. prices have gone up but you agreed a lower price, then your hedge becomes an asset instead.

[xviii] Using the LCCC estimate of contracted supply from AR 1 to 6 and bespoke contracts, and author’s estimate of supply from the AR7 round based on assumed capacity factors.

[xix] Wholesale market prices are above £110 per MWh as of April 2026, which is higher than the 2025 average price and the agreed offshore wind CfD strike prices in early 2026. LCCC.

[xx] The government does contract with batteries, gas, and other facilities via capacity market mechanisms, but this is more about reliability of supply than guaranteeing a price for consumers.

Korea is the extreme version of this experiment. The government freezes retail tariffs on political cycles, and KEPCO absorbs the gap on its balance sheet. Between 2021 and 2023, that cost KEPCO roughly $33 billion in cumulative operating losses.

The pain didn’t stop there. Korea imposed a ceiling on the wholesale price itself, so generators couldn’t pass through fuel costs either. Few private generators had the balance sheet to absorb three years of losses.

That matters now because Korea needs tens of gigawatts of new capacity for semiconductor fabs and data centers, and generators are not rushing to commit capital. Korea already took on the long-dated price risk the UK is debating. The cost wasn’t just KEPCO’s balance sheet. It was the investment cycle that followed.

What great work Lucy.

It puts my work on UK energy market to shame - similar interests - just a different perspective...