The Iran War is Britain’s opening for bold energy reforms

Based in London? You’re invited to my energy podcast launch night at Octopus HQ this Tuesday March 24th from 6.30pm. RSVP here to get on the list. You can already listen to our first few episodes on Apple or Spotify including this week’s episode.

Can you believe the Iran War started just three weeks ago?

Energy costs in Britain have just about doubled in that time. British gas prices jumped within days of the US-Israeli bombing campaign, while oil prices rose more slowly. Prices could rise non-linearly from here as the buffer of oil and gas stocks runs out and governments around the world turn to more extreme measures to manage demand. Much higher prices are likely if the conflict continues, as is a price collapse if the war ends.

The British government faces a crisis painfully similar to the energy shocks brought on by the Ukraine War in 2022. Physical supply disruption is less acute this time because the UK’s consumption is much less exposed to the Middle East[i]. Electricity prices in March are less than half of the 2022 average and less than a quarter of their 2022 peak at the height of the Ukraine War shock[ii]. But prices have already risen enough to potentially increase energy bills up by 12 to 20% in Q3. Government 10-year borrowing costs are now at pre-2008 levels, eating into government budgets and increasing the cost of any support packages.

This time round, the government has even less fiscal room to manoeuvre. They can learn from their predecessors’ mistakes. Like the last major shock, this is an opportunity to push for secure, cheap energy and to reform electricity markets. Britain shouldn’t let it go to waste.

What has the government done so far?

The government’s initial measures announced between March 6th to 15th are not so different from what they were already doing. The assurance on energy bills being protected until the end of June is not an emergency response but just how the quarterly price cap works. Bringing forward the next Contract for Difference (CfD) round, the government’s long-term contracting scheme for renewables, can lock in prices, but can’t help with additional supply as grid capacity is already allocated to 2030 under the recent connections reform. The Fingleton Review reforms for nuclear projects were already ideas on the agenda for renewables, for example cutting environmental assessment duplication, limiting judicial review and consenting projects faster. The Warm Homes Plan announced earlier this year is being fast-tracked in some cities. The government has put companies on alert for price gouging via the Competition and Markets Authority but they cannot do much if companies reflect the market. The UK released a sixth of its emergency oil stockpile, which amounted to just nine days’ worth of domestic demand, and has deferred an increase in fuel tax for drivers by five months.

Its new policies are helpful but unlikely to be sufficient. The government has finally permitted the use of plug-in solar, which saves money on energy bills but only over a multi-year pay-back period and potentially causes unintended price rises for the electricity network[iii]. A newly announced subsidy, £52 million to support 1.5 million households using heating oil, equates to a £35 top-up per home. Oil heating costs that are likely to rise by over 10 to 20 times that amount[iv], though will hopefully be limited by warmer spring weather.

These measures fall far short of the £51 billion support package (2% of GDP) that obliterated government budgets in 2022/23[v] plus a further £11 billion in 2023/24. Only 9% of the 2022/23 cost was offset via energy producer windfall taxes. The announced measures are unlikely to be enough to manage the fall-out that has already happened. Cornwall Insight forecasts that the energy price cap will rise by 12% and 20% from the Q1 and Q2 price caps respectively[vi], and the shock is already affecting food, other consumer products and potentially mortgage payments.

What can the government do next?

This shock could be an opportunity for the government to make the energy system work better by rebalancing electricity and gas prices, reforming markets, supporting long-term contracting, and unlocking more distributed energy assets.

Price rebalancing

Emergency subsidies could work in the short-term but the budget is limited. They also risk disincentivising demand reduction or the switch to cheaper alternatives by dampening price signals.

A more sustainable approach is rebalancing electricity and gas prices. Making electricity cheaper relative to gas and oil products would help to accelerate electrification of transport and heating. Adding carbon taxes to gas or eliminating them from electricity would help but risk causing more political headaches. Shifting an additional ~5 pence per kilowatt-hour of policy costs off bills and onto general taxation is an easier place to start.

Market reform

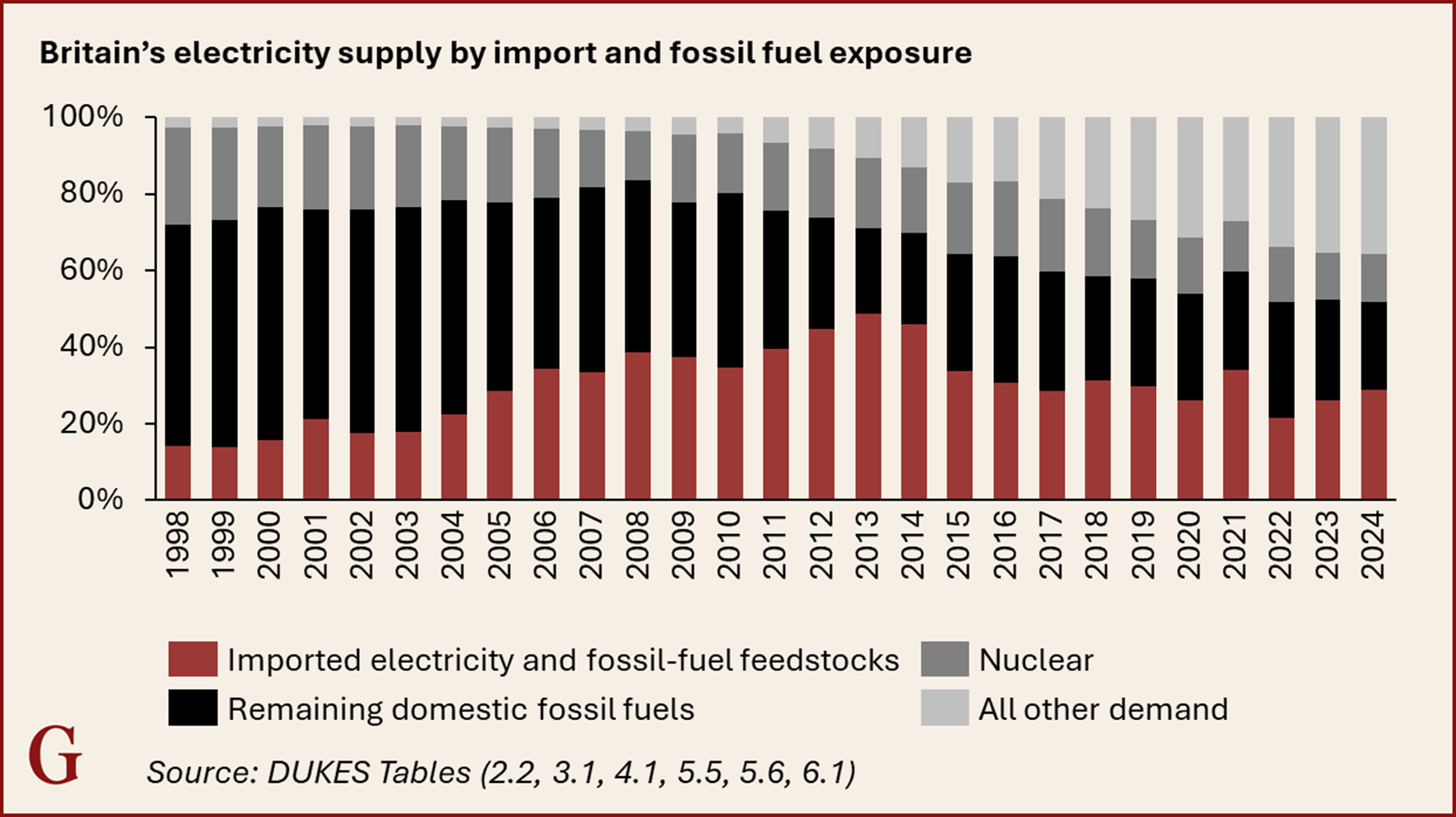

Gas dependency is the primary driver cited for persistently high British energy costs. This is partly because gas is imported and uses an international reference price, and partly because it sets the wholesale market price for all other generation. Although the UK has reduced both its electricity import exposure to 29% (down from 49% in 2013) and fossil fuel use over the past decade, the Energy and Climate Intelligence Unit estimated that gas was setting the wholesale market price 85% of the time in 2024.

The UK’s electricity supply has reduced its exposure to imports since 2013, and fossil fuels over the past two decades

The government could start to address this problem by making the market function properly. The UK’s electricity market takes into account delivery time, but not delivery location. All generators are paid a national price based on the most expensive unit that customers were willing to buy. Once it comes time to deliver the power, some generators are unable to dispatch the electricity they have sold because the grid is too constrained. This is exacerbated when contracted assets bid in the market as close to zero as possible to ensure they are chosen to dispatch, even if their location is constrained.

These distortions lead to wasting curtailed energy, higher network costs to make up supply from other sources, and exporting power at subsidised prices. To give certainty to investors, the government has so far resisted reforming the market to incorporate geographic constraints. But the current system rewards incumbent generators more than it incentivises new renewables investors, who typically rely on contracts to build projects. Regional pricing would send investment signals to build renewables and demand centres in parts of the country that can absorb it.

It should not go so far as separating renewables and gas markets. This doesn’t help all that much as marginal pricing is a market-making mechanism, not unique to energy. Separating out the markets would still lead to participants guessing at the whole-of-market clearing price, leading to less efficient bidding than a combined market. Nationalising gas assets is an interesting twist on the market separation idea, but it only works if governments are willing to operate them with a long-term security perspective.

Long-term contracts

The government could instead fill the long-term contracting gap without major nationalisations. Another reason the UK energy markets are so prone to shocks is the reliance on spot prices instead of contracts. The UK’s consumer protection policies cap prices each quarter while requiring that customers can switch easily between suppliers. People can sign up to fixed-price agreements when they are nervous about prices going up, but switch to another supplier when they see prices coming down again. This disincentivises suppliers to enter into long-term contracts with energy providers and customers alike, as it significantly increases the cost of hedging. The market liquidity for contracts beyond a year or two is thin and most gas generation ends up trading on short term markets.

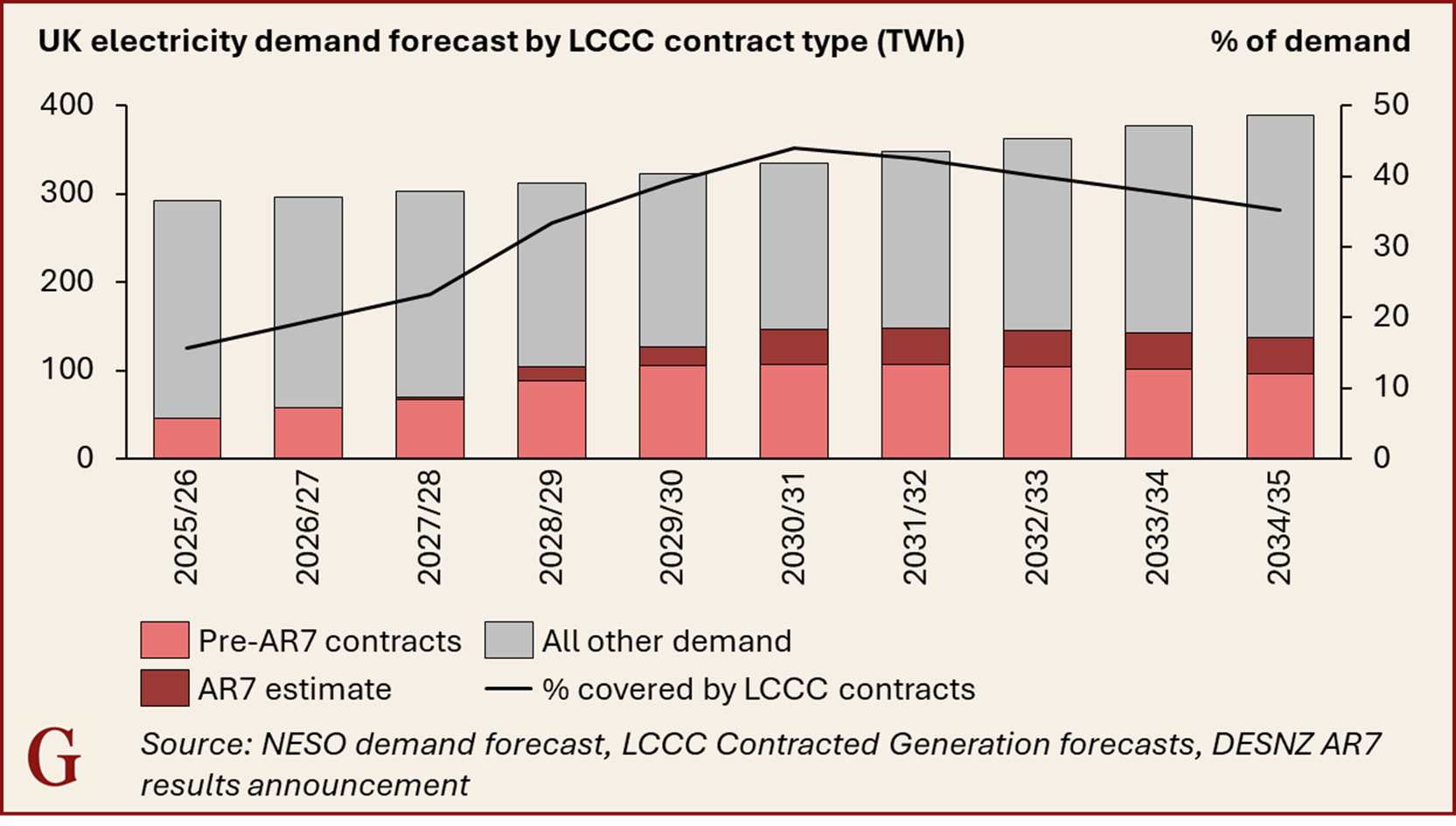

CfDs are notable not just for subsidising renewable electricity, but for offering long-term contracts to generators that the market does not provide. Even if the CfD strike prices are higher or similar to historic wholesale prices, they offer predictability for 15 to 20 years. Based on all the CfDs that have been agreed including the latest round in 2026, the UK electricity market will have 44% of supply on fixed price contracts by 2030/31[vii]. The case for bringing forward the next CfD contracting round is more about price stability for projects in the queue rather than getting new projects built. Even if CfD costs go up by inflation every year, the higher share of generation covered by the subsidy will reduce price volatility dramatically.

The government could offer more price security by backstopping long-term contracts beyond CfDs. This is most expensive to do in the midst of a crisis, but once prices subside the government could consider, for example, offering contracts to operating renewables projects at below-market rates, or negotiating affordable long-term domestic contracts for gas as part of a support package for the North Sea. Supporting additional drilling would not necessarily reduce energy prices significantly according to the Oxford Smith School, but this would support domestic industry if the UK continues to use gas.

Distributed energy tech

The plug-in solar systems that the government has now legalised are the latest evolution in distributed energy, which now includes rooftop solar, home batteries, electric vehicles, heat pumps and demand control for other devices. Controllable loads help to make most use out of renewables by pairing demand and supply at the cheapest times, while distributed generation is currently cheaper than the grid. The problem is that tapping into these benefits is still too difficult for customers and grid operators alike.

70% of households now have a smart meter installed, and aggregators like Axle Energy are enabling some customers to capitalise on flexibility payments. But half-hourly billing directly at the household level is not yet widely available and not all high-demand devices like EVs and heat pumps are required to be dynamically controllable. The government could mandate that more devices have the option for dynamic controls based on electricity price signals from smart meters, enabling more people to benefit. Requiring data sharing from smart meters to the electricity system operator, NESO, would also provide more visibility on behind-the-meter devices when forecasting grid balancing requirements and costs.

Never let a crisis go to waste

The government is so fiscally constrained that the Ukraine War level of support is unlikely to be feasible this time without significantly driving up borrowing costs. Subsidies can also delay much-needed reforms that could prepare Britain to unlock cheaper electricity. The last government didn’t act nearly enough after the last crisis to secure energy supply and deliver infrastructure investment. Heat pumps still have incredibly low installation rates, electric vehicles are not yet the dominant vehicle choice, gas storage is perilously low, and electricity prices remain high particularly compared to gas.

The current government has so far prioritised net zero investment, drumming up interest in large-scale infrastructure nuclear and renewable projects. It has not yet tackled major regulatory reforms. If we are going to experience a painful period of price inflation and high interest rates, then let’s at least use this opportunity for bolder change, like removing policy costs from electricity, reforming markets to include geographical constraints, contracting supply for longer, and supporting the uptake of flexible technologies. You never want a crisis to go to waste[viii].

If you enjoyed this piece, join 800+ followers in 48+ countries and subscribe for regular long-reads on the energy transition. Please share it with friends and colleagues, and leave a comment with your thoughts.

[i] 49% of British gas was imported in 2024, of which most comes from Denmark – around 2% of total gas consumption came from Qatar (Parliamentary briefing). Oil is more exposed to the Middle East – less than 2% of primary oil product imports come from the Middle East but 27% of petroleum products for a total of ~12% of all oil imports in 2024 (DUKES 3.7)

[ii] The time-average wholesale price for March is £96 per MWh compared to £205 per MWh for 2022 (LCCC Intermittent Market Reference Price as proxy for wholesale prices).

[iii] Behind-the-meter solar is not visible or controllable for NESO, the electricity system operator, and reduces their ability to plan for energy supply including balancing. Using rooftop solar, whether plug-in or fixed systems, reduces the amount of network electricity purchases, which could spread network charges over fewer units and raise prices.

[iv] Heating oil prices doubled from 65 per litre to over 120p per litre since the start of the Iran War, and households with oil-based heating systems use over 1,500 litres per year. As the pre-war cost is estimated at ~£1,000 per year and looks set to double. The increase is at least 20 times the £35 top-up but potentially much higher. In Northern Ireland, the bill impact is estimated at an additional ~£500, or 14 times the top-up payment.

[v] £200 bill discount to all households, £150 council tax rebates, 5p fuel duty cut, cost-of-living payment to some households, energy price guarantees of £23 billion, bill relief for businesses of £7 billion and more.

[vi] Cornwall Insight as of ‘close of play’, 19th March 2026. Price cap forecast was £1,972.53 for Q3, against the Q2 2026 price cap of £1,641.

[vii] Author’s calculations using AR7 results project announcement tables and assumed capacity factors, and the LCCC’s estimate of future contracted generation as of March 2025.

[viii] Rahm Emanuel, 2008. Also attributed to Winston Churchill but this is unverified.