Death by a thousand cuts: is there any hope for lower electricity bills in Britain?

This is the third part in a series on UK electricity prices. Part one discussed what 2025 told us about gas setting the price of electricity. Part two explored the role of contracts for insurance vs cost reduction, and whether renewables need them.

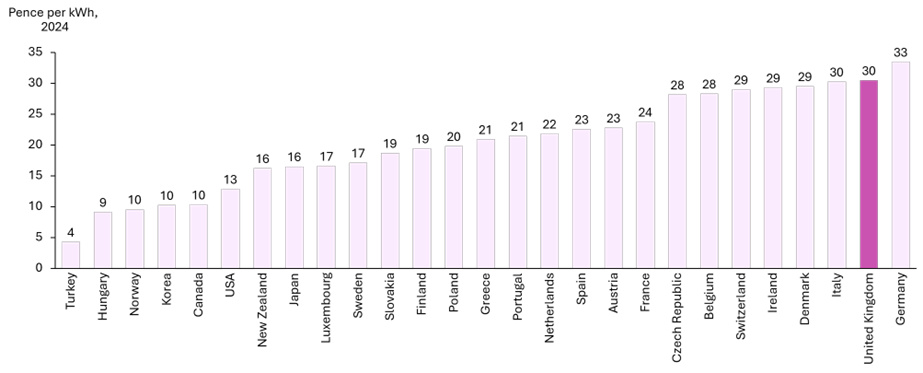

The UK is a world leader in high electricity costs and I am constantly asked why. I am hard-pressed to identify one single cause. The cost of generating electricity has risen, especially since the Ukraine War, but so has the other two thirds of the energy bill. I’m even harder pressed to identify a silver-bullet solution to bring down costs.

Domestic electricity prices by country, 2024

Why are British electricity costs high?

I have a few theories about why electricity prices are high in Britain.

The UK generally is a highly liberalised and privatised electricity market. This alone can partially explain Britain’s high prices. A private sector owner is likely to extract more profit and have higher financing costs, which could outweigh any efficiency gains relative to a state-owned company.

Interconnected grids also reduce cost by allowing electricity to flow freely between demand and supply centres. As an island, Britain has lower interconnection than mainland Europe, and it has bottlenecks throughout its transmission system. Low-cost generation cannot always be dispatched where it is needed, increasing system costs.

Generation (wholesale) costs make up about a third of the UK’s electricity bill. These went up due to gas price spikes but are also generally high in the UK because construction is more expensive. This is driven by planning restrictions, environmental surveys, safety regulations, grid connection delays, and more.

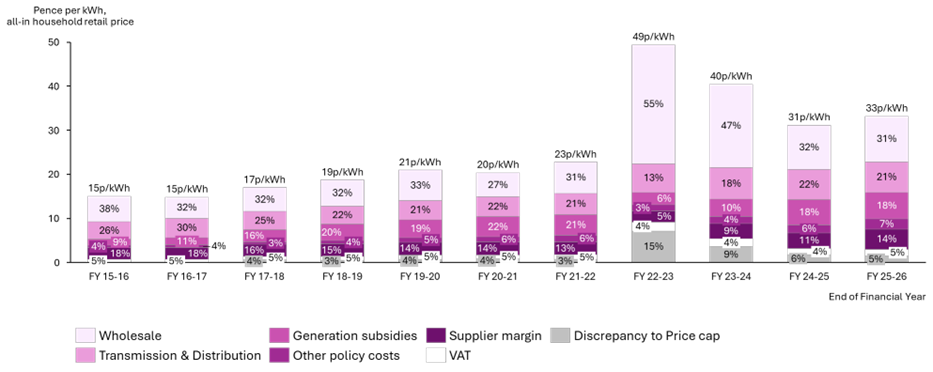

Price cap unit electricity prices by bill component, by financial year

The remaining two thirds come from network costs, subsidies and other government policy choices, supplier margins, and tax. Network costs and subsidies have both risen dramatically due to the build-out of renewable energy and balancing the grid. This was compounded by broader inflation, which is baked into network revenue and subsidy payments.

Even if wholesale costs fall by half to pre-Ukraine war levels, the UK would still need to bring down the rest of the costs to get anywhere close to historic levels or a regionally competitive electricity price[1].

Costs are likely to continue rising

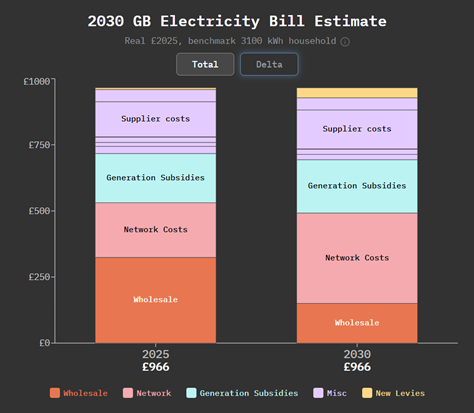

Electricity bills are set to rise even more over the next five years, mainly driven by network costs and levies. Transmission alone is expected to cost 50% more in 2026/27 than in the prior financial year. New levies, like the funding for Sizewell C, will add further costs. This is offset by the hope of lower wholesale prices from renewable energy, and smaller generation subsidies as legacy programs like Renewable Obligations phase out. Unless wholesale costs decrease by more than 50% to £0.039 per kWh (2025 prices), analysis by Ben James suggests that all-in electricity prices are projected to stay the same or go up in real terms by 2030[2].

An estimate of electricity bill price rises, 2025 to 2030

Cost reduction by a thousand cuts

Focusing on wholesale prices alone won’t solve Britain’s electricity cost problem. Indeed, trawling through Ofgem and NESO data is a demoralising experience for anyone trying to identify ways to decrease energy bills. Chipping away at each bill component offers some hope[3].

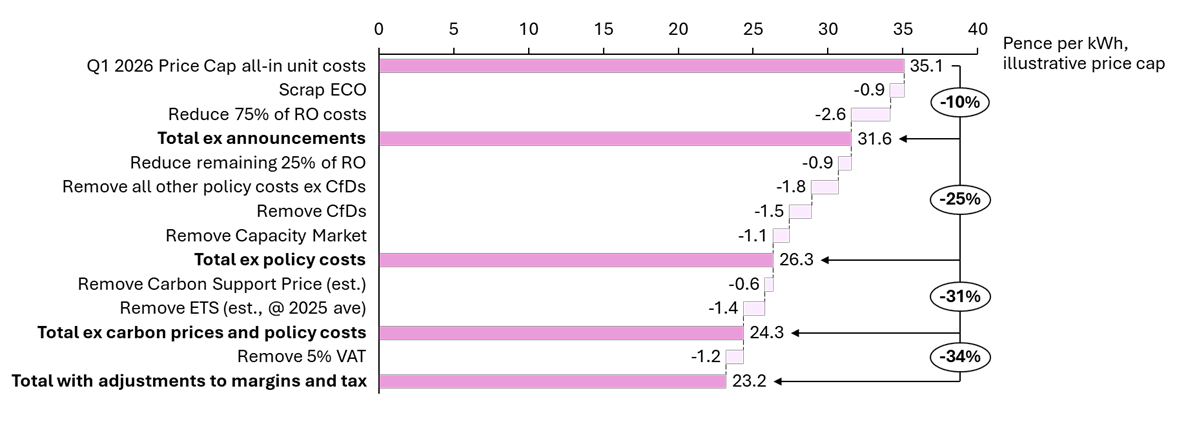

Small cuts to policy costs in the short term can reduce bills and restore faith in government’s net zero and cost pledges. The government recognised this with their Autumn budget announcement to move 75% of Renewable Obligation (RO) subsidies off of bills, and end the Energy Company Obligation (ECO) efficiency scheme.

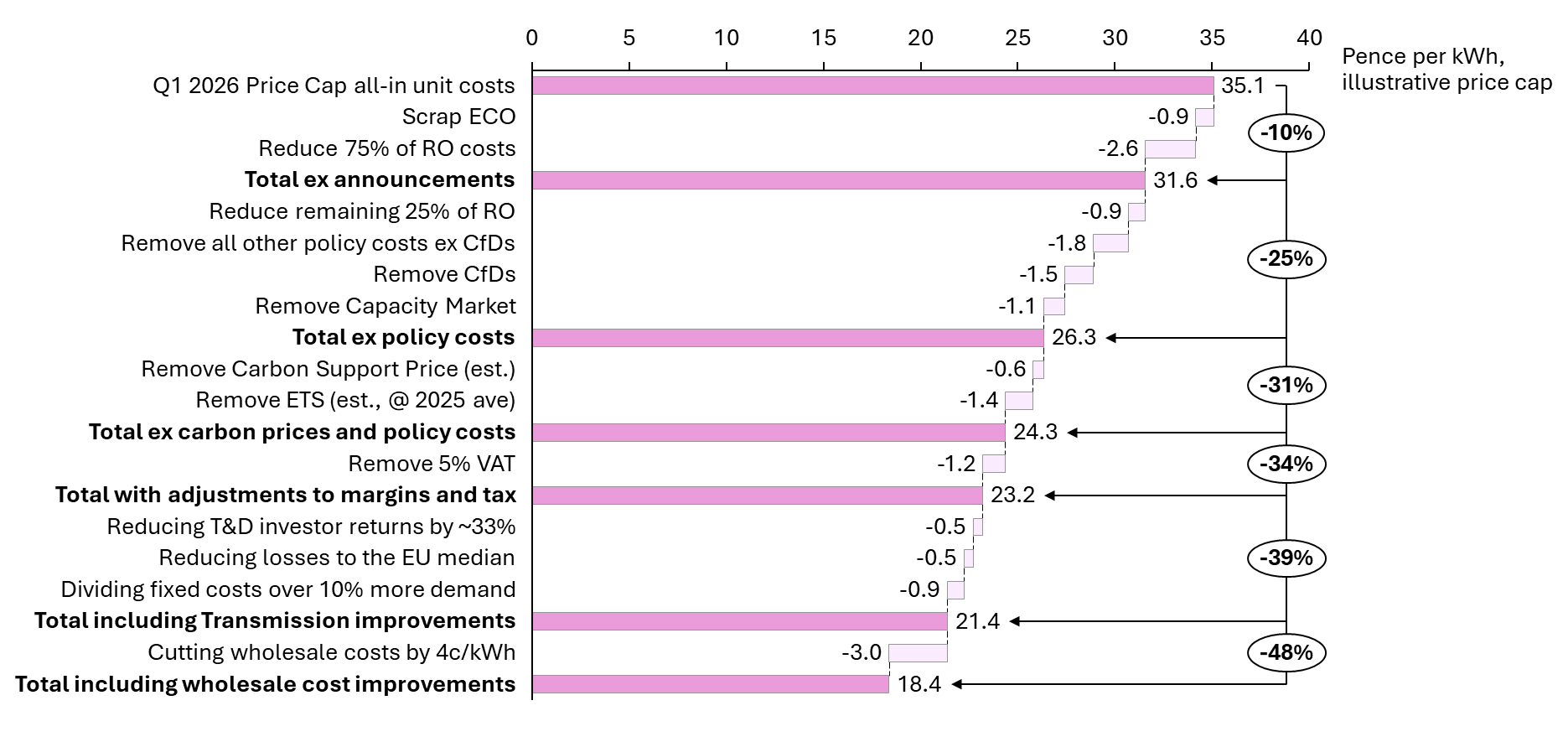

Eliminating policy costs from the bill entirely would reduce unit costs by an estimated 25%. In an illustrative analysis using the all-in unit costs (variable plus standing charges) from the latest Q1 2026 price cap, prices would fall from 35p per kWh to 26p per kWh, including the existing policy to scrap ECO and shift RO costs. This would help the government meet its pledge to deliver lower electricity bills. Unless they repeal these policies, which are increasingly about ensuring energy security rather than subsidising new technologies, these costs won’t go away[4]. Shuffling them to the Treasury may not be practical in the long-term, but it is expedient.

Illustrative bill reductions from the Q1 2026 price cap from policy cost decisions

A popular policy on the right is to scrap carbon taxes. When gas is the marginal price setter, wholesale prices for all bidders include carbon costs, so scrapping the tax would have an impact beyond the carbon-intensive generators. This would reduce bills by another 6 percentage points, or an estimated 2p per kWh depending on carbon prices and how often gas sets the marginal price[5].

Like shifting policy costs, this bill saving would cost the Treasury. The Emissions Trading Scheme is expected to generate £2.6 billion in 2025/26 plus ~£400 million (2024/25) from the Carbon Support Price[6]. Changing the UK’s climate commitments would also affect energy investors’ ability to underwrite projects, if they perceive higher risks from government policy changes. It could come back to bite the UK in trade agreements with the EU, particularly the Carbon Border Adjustment Mechanism. For the avoidance of doubt, I do not support scrapping carbon prices in the UK.

These changes combined with VAT could bring bills down by 28% to 34% depending on if the carbon price remains, before tackling network, wholesale or supplier costs.

Tackling network costs

I started researching this piece by looking at just transmission and distribution costs. Most media coverage focuses on the cost of generation, subsidies, and increasingly, balancing. I wanted to estimate the impact of bold ideas to re-nationalise the grid, reduce network losses, or spread fixed costs over more demand. My high-level analysis suggests they have a surprisingly small impact on energy bills in the short term. This is partly because they only make up one sixth of the bill in the first place[7], though this figure is set to rise, and also perhaps because my assumptions are conservative.

Transmission and distribution companies, collectively networks, are privately owned in the UK. They were privatised in the Thatcher era to unleash private sector efficiency on improving the grid[8]. Nowadays, network profits are dictated by a Regulated Asset Base formula to avoid utilities taking advantage of customers with their monopolistic service. Networks can charge for operational expenses, replacement costs associated with depreciation, and a guaranteed return on their assets[9].

Since privatisation, networks have delivered significant returns to shareholders. Bringing networks back under public ownership could reduce costs because government borrowing rates are lower than private capital costs. Regulatory hijinks aside[10], investment returns are supposed to make up between 20 to 30% of network company base revenue in regulatory models. Refinancing the allowed revenue at today’s government long-term interest rates, around 4 to 5%, would reduce returns by around a third[11]. Applying these savings to Distribution and Transmission costs on the price cap saves around 0.5p per kWh[12], an order of magnitude lower than estimates from a 2019 study with a different methodology[13]. Nationalising may have other benefits if it can accelerate grid investment, but reducing financing costs alone doesn’t seem worth the political upheaval of changing ownership[14].

The UK also has high transmission and distribution losses relative to Europe. In 2024, losses were 8.9% of total British public distribution system demand[15], versus the European median of 5.6% in 2022. If losses went down to the European median, variable electricity costs could fall by ~3.5% from the efficiency gain. At least 60% of the electricity bill was variable in Q1 2026, so this could deliver another 0.5p per kWh in savings. This would probably require some capital investment, which may be too high to offset any benefits.

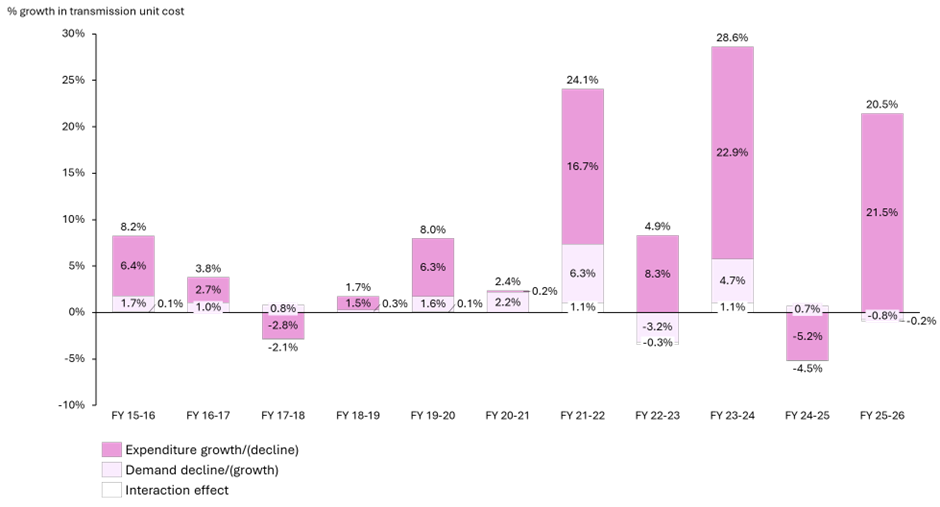

The UK’s transmission and distribution systems have high fixed costs and are spread over a diminishing base of demand. Transmission costs have increased in absolute terms, but they have grown even more per unit. Allowed revenue for the transmission system, a proxy for costs[16], rose by 93% between FY16 and FY26. Over this same period, electricity consumption from the distribution network fell 12%[17]. These factors combined led to a 120% growth in unit transmission costs[18].

Estimated change in transmission unit cost, split by expenditure and demand drivers

2025 was the first year that electricity demand rose in a decade, barring the post-COVID rebound. The network has expanded in that time to accommodate more connections. If electricity demand increased, unit network costs could go down, starting a virtuous cycle of cost declines from higher utilisation of network infrastructure. With 10% higher demand, network costs could fall on a unit basis by up to ~0.9p per kWh if all network costs were fixed. This small reduction is unlikely to drive much of a flywheel effect in the absence of other price cuts.

Even more illustrative bill reductions from the Q1 2026 price cap based on policy cost decisions, network changes and wholesale cost reductions

And the rest?

I did this exercise primarily to understand the relative magnitude of a few different solutions to reduce electricity bills beyond bringing down wholesale costs. There are countless other policies I did not consider in this analysis, and the analysis I did was at a high level with assumptions that could be debated. These estimates are very rough and I do not support implementing all these options. Different changes could interact with each other, for example moving so much cost to central budgets could have unintended consequences if it causes demand for electricity to increase dramatically.

Reducing wholesale prices by half from 2025 would be a bigger prize than any of these other changes, around 3p per kWh net of carbon price reductions[19]. This could support a cumulative bill reduction of almost 50% inclusive of all the illustrative cuts (noting again that I do not support scrapping carbon prices and that these cuts do not necessarily reduce system costs but change who pays).

Bringing down wholesale costs is a function of cost of capital, build costs, and market design. The decline in renewable technology input costs (e.g. for battery and solar) has been promising internationally, but the UK’s solar install costs were 24% higher than neighbouring Ireland in 2023. By 2024, the UK’s offshore wind capex was 4% higher than Europe averages, and 42% higher than Asia, and onshore wind was the highest cost in the top markets covered by IRENA. Focusing on speeding up grid connections and construction, and bringing down build costs could drive meaningful savings.

Reforming markets could help to capture some of the upside of lower energy costs, by reflecting geographic constraints in pricing. Increasing flexible technologies like batteries, Electric Vehicles, and heat pumps could reduce the requirements for grid build-out if they can participate fully in the market. At the right electricity price, this would also reduce total energy bills by switching from gas or petrol to electric.

By laying out these options, I have found hope in the political possibilities of reducing bills. Reducing real costs is more challenging. In my view, tinkering with markets and ownership structures might help to make British energy prices more competitive. But it is essential that the UK reduces the cost of building energy infrastructure and the uptake of flexible technology to reduce investment needs in the network. I don’t see how energy costs can fall meaningfully without changing how and what we build.

Subscribe to read more about UK energy, and international stories on coal and the energy transition. Read on for a bumper list of footnotes.

[1] Though to be fair, my analysis focuses on household electricity bills and not industrial prices – what we usually think of when we think about “competing” on energy prices.

[2] Ofgem has representative consumption coming down for the average household to 2,700 kWh per year as of November 2025. This number may go up as more households adopt electric heating and vehicles so I tend to focus on unit costs rather than bills.

[3] As does Ofgem’s decision to make bills appear a bit lower by reducing the amount of electricity it thinks households use.

[4] Except for the scrapped ECO.

[5] The Carbon Support Price is fixed at £18 per tonne, and the Emissions Trading Scheme price fluctuates with the market (£49 per tonne in 2025 and £68 per tonne in January 2026). Gas is estimated to set the price 85% of the time as of 2024 and less in future. Much of the market is also contracted by CfDs or over the counter contracts. A conservative estimate of cost reduction potential would add these two factors together (as in CBP analysis), but in reality the CfD delivery times have some correlation with the times when gas is setting the price so savings may higher.

[7] Ofgem price cap, Q1 2026, TNuoS and DNuoS as a percentage of total bills.

[8] Whether this has happened is debatable – read Arthur Downing’s work to learn more.

[9] These are the main buckets, there other revenue items like pass-throughs and performance incentives.

[10] Investors optimise each regulatory cycle to increase returns, for example adding more leverage than the regulated returns compensate for, or re-financing at lower rates. These loopholes are sometimes closed in the next cycle.

[11] Returns for electricity networks are ~3.5% to 4% real WACC, plus inflation at 2.5% to 3.5%. If government financing is at 4 to 5%, this represents a saving of 2 percentage points.

[12] Using per kWh TNuoS and DNuoS costs on the Ofgem price cap, weighted average by region, applying their respective percentages of returns as a percentage of base revenue in FY26 (27% and 24%) and reducing this cost by one third (~4.3% to ~5.1% long-term government gilt rates versus ~6.3% to ~7.5% inflation-adjusted WACC).

[13] Multiplying 0.5p per kWh x 2,700 kWh of demand = ~£13 per customer saved. The study estimates savings of £142 per household from nationalising electricity grids. Partly this is because this was a low rates environment, but it also is a difference in methodology. I have looked at the allowed returns of electricity companies, rather than their dividends. I have also not assumed any reduction in revenue from remunerating depreciation. The author also assumes total financing costs are ~£5 billion across network companies in future, which seems high considering allowed revenue for T&D companies in 2025/26 is £11.9 billion.

[14] Networks also deliver outsized returns relative to their regulated returns in part because of re-financing beyond regulatory limits and because they can claim depreciation as a cash benefit even if not investing that level of maintenance capex.

[15] DUKES 5.2.

[16] This is an imperfect proxy that covers all generation, not just households. It is derived from allowed revenue for the Transmission companies, less connection revenue, and adding offshore transmission revenue. Allowed Revenue is consistently published by NESO and TNuoS costs feature in the consumer bill Price Cap.

[17] Using calendar year 2024 instead of FY2024-25 for the 2025 estimate.

[18] This will look different from the changes in the TNuoS section of the domestic price cap for a few reasons (possibly more). Transmission costs are levied on both generators and end customers, so a small portion of transmission cost is embedded in wholesale prices. The price cap was using the same per-household demand for the past 10 years (3,100 kWh), only reducing it in January 2026 (2,700 kWh).

[19] Wholesale price allowances on the bill are more like 10p per kWh, possibly because of contracts outside wholesale markets and higher anticipated costs in Q1 2026 compared to calendar year 2025. ~3p per kWh avoids double-counting the carbon price reduction.

Carbon tax is impacting pricing heavily as gas sets the price most settlement periods so removing it lowers the cost. Yes the Treasury might lose the income but lower energy costs would feed through into higher growth so they would make it back elsewhere. On Networks we are already under provided for renewables we have on the network today due to daft connect & manage policy so the buildout to 2030 needs to happen. What happens after then should be revisited.

To Ms. Shaw: -- the "fix" for this -- is being privately developed for mass use - in the form of a small, solid-state , electric power supply - which a Physicist in the UK has tested, and published that the sysem he built developed a 9 :1 output to input power ratio - with laboratory size testing.

His system is sized to develop the single-phase / 230 AC / 50 Hz / 20 Amp power commonly used in the UK - and with larger components can develop up to and including 480 VDC or VAC / 600 Amps / 288 kW max - or 400 VDC / 600 Amps for vehicular power.

The technical information - labeled "MRES" - can be found on the website "Kerrow Energetics" / owned by Physicist and Electric Power Researcher, Mr. Julian Perry.

The technology is using the exact same resonating electric circuit, used exactly the same way - as the resonating receiver circuit found in the billions of radios manufactured after Nikola Tesla invented the Radio in 1900.

It should be pointed out - that presently there is no Law or Regulation that stipulates that any private premises owner (of any size premises) if connected to a power source - has to use "only that power made available" by that connected power source.

It should be pointed out that the unit can be installed either singularly, or in numbers required to continuously power any site - up to and including any "heat-sourced" (including Atomic of Fusion if one ever gets built) or Hydro-powered high voltage electric power station - allowing for all now clean power plants to be used 24-7 / 365 days a year / at up to 100% continuous output.

It should be pointed out that as far as vehicular power - any battery or ICE (internal combustion engine) powered vehicle, can be retrofitted-repowered, be it on land / in or on the seas / of in the air as a propeller; rotor; or hi-bypass jet powered private of commercial aircraft - making available:

--- unlimited range of travel and / or movement, and

--- unlimited time of travel and / or movement.

Finally -- it should be pointed out that in 2024, just after the Labour Party was voted into office: the technology was directly offered, "with no strings attached" to: PM Starmer; Exchequer Reeves; Secretary of Energy Miliband; and Mission Control Chief Chris Stark - who asked for and received the information via LinkedIn - and then "went silent".

The others did not respond.

The Governments of Wales and Scotland also received and positively reacted to the information - with the caveat "...that Westminster controlled the power sources and the power grids..." (paraphrase).

So you now have it.

What you do with the information is up to you - because the power units will be available in the future.