If renewable energy is cheap, why would we contract above traded prices?

The cost of insuring against volatility may offset the benefits of reducing the cost of capital.

This is Part 2 of a series on electricity prices in the UK. Part 1 explored what 2025 told us about gas setting the price of electricity. The next in this series will look at transmission & distribution costs.

High prices cure high prices. This is a comforting maxim in commodities markets, because it suggests that price spikes won’t last long. Investors develop new supplies while a commodity is expensive, and prices come down as this production comes online. Similarly, when prices are low, investment in high-cost production stops, eventually raising prices again.

This phenomenon has not quite translated to Britain’s electricity market[1]. Renewable energy is supposed to be cheap. If prices are high, this should be a boon for those providers, unleashing a flood of investment. Indeed, several projects have come online, and a record number are in the pipeline. Yet renewables developers still want a government backstop for prices. Why?

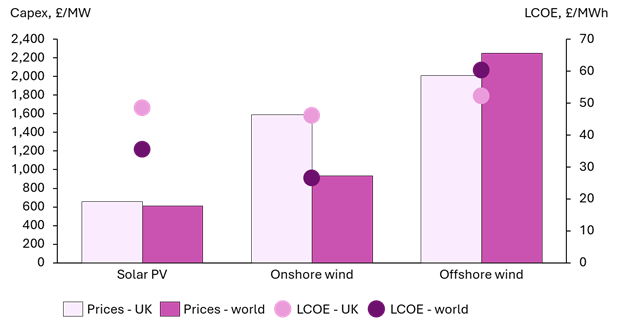

The simplest answer would be that renewable energy isn’t cheap after all. Building both solar and onshore wind is more expensive in the UK than globally. The UK has similar or higher wind resource than the world average, while solar is lower. Even though the UK may benefit from lower cost of capital than other countries, British solar and onshore wind has a high levelised cost of electricity (LCOE), a theoretical measure for the cost of generating a unit of electricity over its project life. This calculation is highly sensitive to capital expenditure and cost of capital, which has risen since the UK figures were calculated[2]. Although the quoted LCOEs are lower than current wholesale prices, they may not be representative of current costs[3].

Capital cost (£/MW) and Levelised Cost of Electricity (£/MWh) by technology, 2023 figures and prices

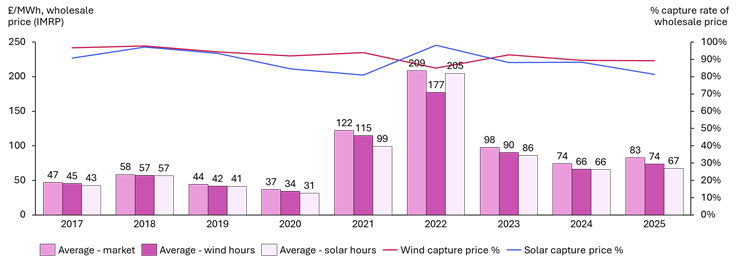

Another simple answer is that renewables capture a lower price than the rest of the market. This was certainly doing the rounds on the conference circuit in 2025, driven by high solar production in Europe. When renewables are generating at the same time due to correlated weather events, this brings down prices. This is partly because renewables are a low-marginal cost source of energy, and partly because if projects have a contract or a subsidy, they can bid close to zero and still be paid well[4]. This discount is real but not catastrophic in the UK because the prevailing market price is so high. Solar and wind capturing ~80% to ~90% of the average wholesale price (£67 to £74 per MWh in 2025) is still higher than Arup’s estimate of British wholesale costs and is on par with current contracted prices[5].

Capture prices of wind and solar relative to wholesale prices by year

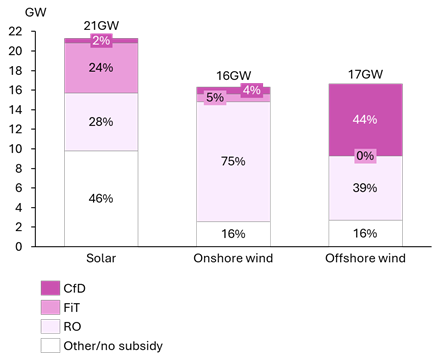

Which brings us to the purpose of government contracts for electricity. As much as ~46% of solar and ~16% of wind capacity[6] in the UK is not supported by the government’s flagship subsidy and contract schemes[7], suggesting at least some have been financed outside these channels. Let’s assume that renewable energy can be built cheaply enough to beat gas prices[8], and that they will still make enough money on wholesale markets even with the discount. What, then, is the incentive to contract for each counterparty?

Percent of renewables capacity by support mechanism

Conventional wisdom is that government-backed contracts for renewable energy reduce costs by reducing risk. In the UK, the government supports renewable energy with Contracts for Difference (CfDs)[9], which guarantees projects an inflation-adjusted price for 15 to 20 years[10]. The contract reduces revenue risk, which in turn reduces the investment return for debt and equity that financiers are willing to accept to fund the project. When almost all the cost of renewable energy is up-front, this directly translates into reducing unit costs. Depending on how competitive the market is and how this saving is shared, it is a win for both investors and consumers.

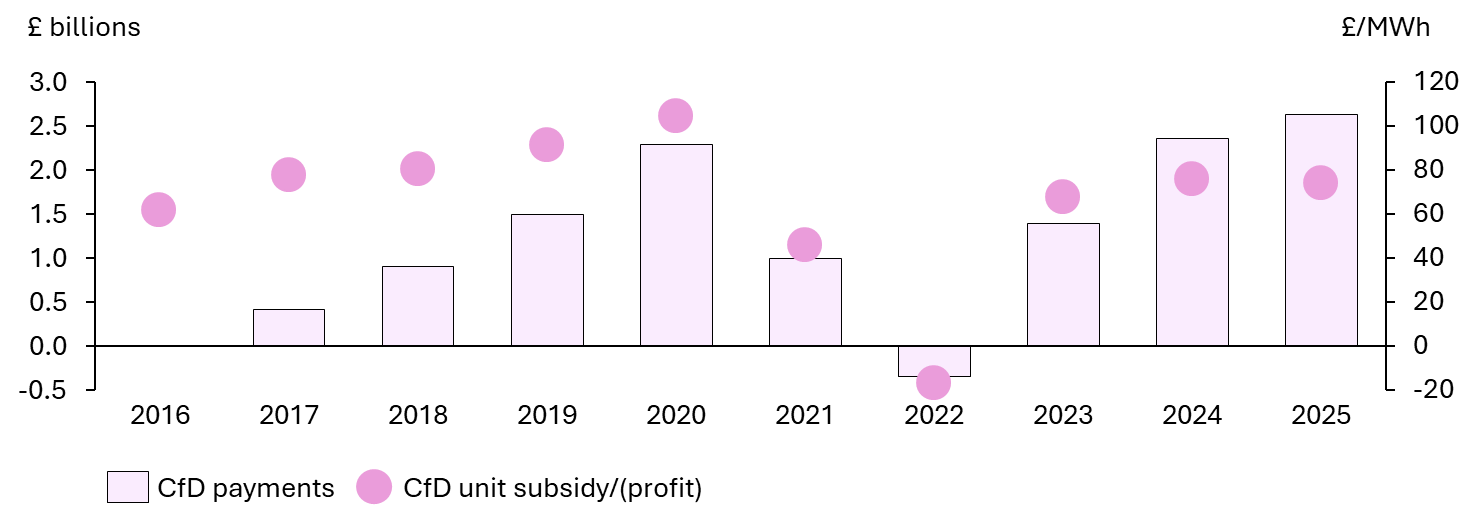

This capital-cost-reduction benefit has not yet translated to cheaper prices, in part because earlier CfDs were primarily a subsidy to support renewables. Over £12 billion has been paid to CfD holders since 2017, or ~£66 per MWh. Just one year yielded a net gain to the government: 2022 when energy prices skyrocketed. Newer solar projects [11] returned over £1 billion to the government in 2025, but the vast majority of the low-cost CfDs have yet to be built. There could be a big surplus in future, but inflation may erode new CfD cost advantages by the time projects come online.

Total payments and subsidies/(surplus) to CfD generators over time

What if another benefit of these government contracts was important: hedging. Buyers may want to insulate themselves from rising prices and are willing to pay a premium. Sellers may want to lock in prices now in case they fall in future.

The power of each counterparty dictates who profits most from the trade[12]. In a market with falling prices and big returns to reducing the cost of capital from contracts, I would expect incredibly competitive bidding from the private sector. I suspect that the government now has more to lose than the energy developers, and may pay up to insure against price rises.

Whenever I’ve spoken to veteran power sector investors and traders, they hold a belief that wholesale prices will be lower than forecast and certainly wouldn’t go up with inflation. This may be a conservative view that makes their deals look more profitable than they originally planned, or it may reflect lived experience of being burned by wholesale power markets. Investors who believe that wholesale prices will go down, and who receive a reduction in capital costs for fixing prices, are more likely to keep their CfD bids low. Their counterparty would then reduce their volatility and short-term prices but lose out on the benefit of wholesale prices going down in future.

What’s happening now is the opposite. Demand is increasing for the first time in decades, and likely to go up further with the rise data centres, and electric vehicles and heating. The additional infrastructure investment required to meet this demand is huge and takes time. Households and businesses have been strained by price shocks that they expect the government to protect them from in future. The government has a lot to deliver at once: sufficient electricity, at a reasonable price, with low volatility.

This places the government in a less powerful position. They want to guarantee the price for a large amount of newly built electricity generation, and demand is growing. Even though the government is reforming planning and clearing out the grid connection queue, building enough power at pace to meet demand and reduce gas power on the grid will be tough. If supply can’t keep up, wholesale costs will rise. The government could adjust taxation to ensure this price increase won’t affect consumers, but it would still need to be funded as part of the overall budget.

When prices are rising, or there is uncertainty, the opportunity cost for an investor is higher. Think about how mortgage rates go up for longer loans, unless the bank thinks rates are going to fall in future. Developers might charge a premium on wholesale prices to fix their revenue, rather than a discount. The government might end up locking in higher prices for electricity, not necessarily because the cost to build is higher, but because developers know the government values risk reduction and they can profit from it.

The latest CfD auction results are out this week and in early February. If they are higher than prevailing wholesale prices[13], the government will need to explain why cheap renewable energy isn’t delivering. There may be other drivers of this, like higher build and financing costs or an insufficient supply of sites. Bringing down construction costs should remain a government priority.

But the answer may also be that volatility management matters more than lower prices. Prices may go up because the government wants to buy insurance, not because renewables are expensive. If that is the case, the government needs to say so. Otherwise, they risk misleading voters about what contracting electricity is really for. This could put the public off “costly” renewable technology even if it is the best way to deliver energy security for Britain.

Subscribe for more updates on the energy transition in the UK and around the world. Drop a comment with your thoughts or hit reply to this email.

[1] Wholesale and retail prices have come down since their price spikes before and during the Ukraine war but they have not settled to pre-war levels. This reduction is primarily due to gas prices settling.

[2] Arup estimates this at between 5 to 5.8% WACC, while CEPA analysis estimates this at 7.6% WACC, both pre-tax real figures.

[3] The LCOEs are also calculated using real pre-tax cost of capital, which is different from post-tax nominal cost of capital.

[4] Later auctions prevent being paid if the market price falls below £0.

[5] The wholesale capture prices shown in the chart are spread across all generated units. The prices for Contract for Difference are for delivered units, which accounts for any times of day when power prices are negative and the project cannot receive payment for its contract.

[6] Range due to potential projects covered under ROs built after the RO annual report date. This impact may be small as ROs closed to new projects in 2017.

[7] Contract for Difference, Renewable Obligation Credits and Feed-in Tariffs.

[8] A BIG assumption – I suspect the cost to build renewables is not cheaper on average compared to gas but is cheaper in volatile years and once projects stop being contracted. Maybe this is worth it – but we won’t get that benefit for 15-20 years.

[9] There are numerous other ways the government supports renewable energy, including carbon prices and other subsidies.

[10] Older contracts last 15 years, newer contracts last 20 years.

[11] Rounds 4 and 5.

[12] As well as strong competition between parties on the same side of the trade.

[13] Or likely to be by the time they come online.

"British solar and onshore wind has a high levelised cost of electricity (LCOE), a theoretical measure for the cost of generating a unit of electricity over its project life" -- but lower than all the alternatives.

"The latest CfD auction results are out this week and in early February. If they are higher than prevailing wholesale prices" -- what's the median age of a CCGT in Great Britain, and what's the median age of a GB nuclear reactor? Do you think they are still paying off the finance raised to construct them, and that cost is reflected in their market offer price? Do you think the existing CCGT and nuclear fleet can operate indefinitely without replacement?

the governments new angle pre ME crisis was new build renewables are cheaper than new build gas plants so it doesnt matter that the prices have gone up.