What 2025 prices really tell us about "gas setting the price of electricity"

This is part one of a series on electricity prices in the UK. Part two will focus on whether renewables projects are viable without CfDs.

“Gas sets the price of electricity” might just have been the most popular British energy commentary of 2025[1]. This insight offers a simple solution to policy-makers: push gas out of the market to bring down energy bills.

Britain is pushing a massive renewable and nuclear construction agenda, backed by government contracts. But whether gas sets the wholesale price or not is less relevant in a market where an increasing share of electricity has locked-in prices. Contracting so much power may end up counter-productive to reducing cost even if it decreases volatility.

The original claim that gas sets electricity prices comes from a study in 2023, using data from 2021. In Europe, electricity is traded on wholesale markets in increments of time. The most expensive generator that meets the last unit of demand sets the price for every provider for that period. The study highlighted that in the UK, fossil fuels (read: gas) set the power price 97% of the time in 2021, excluding the worst of the gas shortage caused by the war in Ukraine[2]. In the rest of Europe, this rate is much lower, for example just 7% in France and 58% EU-wide[3]. The UK has much higher electricity prices than this peer group, so gas setting its price is presumably a driving factor.

% of time that fossil fuels set the wholesale price: 97% in the UK in 2021

This statistic isn’t as powerful as it first seems, despite being picked up with zeal in 2025[4]. The methodology itself is an approximation based on the change in bidding behaviour between different time periods. It does not actually track which unit was the marginal producer. ECIU reckon the percentage fell to 85% by 2024, but gas still delivered power in 100% of bidding hours. This statistic implies it is not the most expensive generator at least 15% of the time on short-time wholesale markets or that it isn’t bidding at all. Only 34% of electricity was traded intra-day in the UK according to the study and even less elsewhere. Day-ahead markets, private power purchase agreements (PPAs) and long-term inflation-linked contracts like the government’s Contract for Difference (CfDs) scheme drive a large portion of the electricity price.

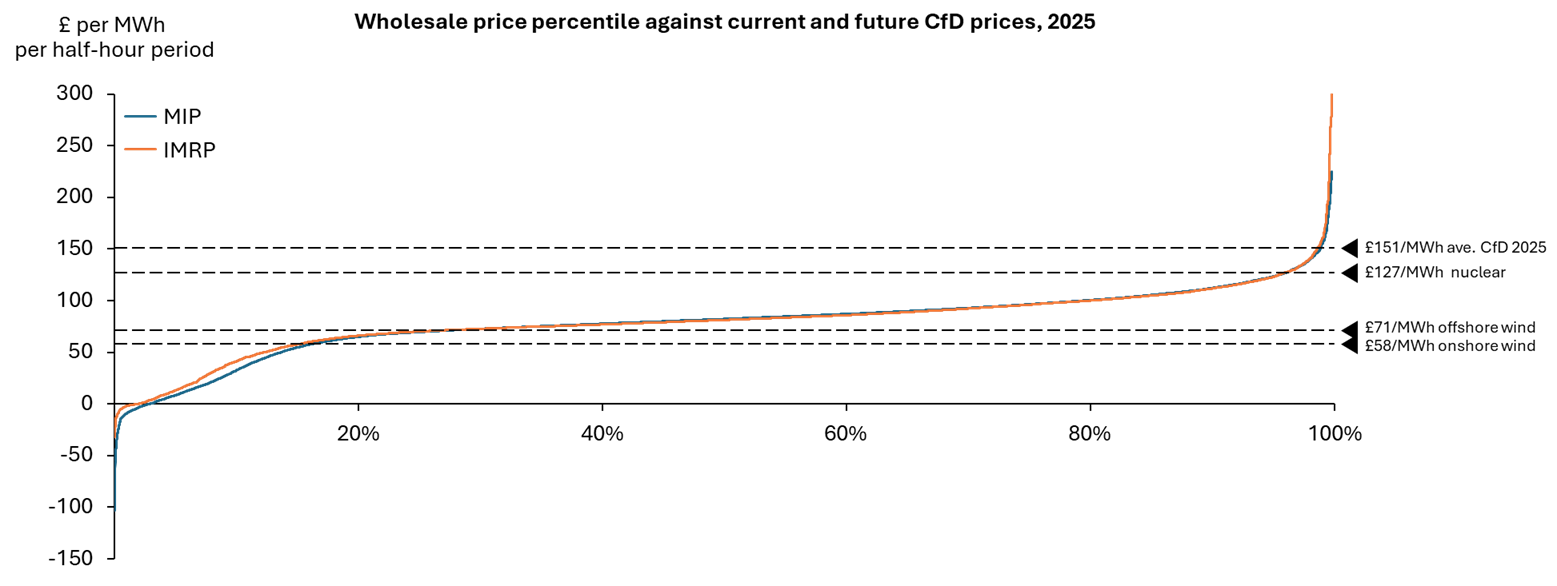

CfD contracts mean reducing gas on the grid may not be sufficient to bring down prices. Generators with a CfD are incentivised to bid wholesale prices close to zero because they are paid a fixed price regardless. The traded wholesale price may be lower, but the all-in cost of CfDs is added elsewhere to the bill. Gas can become the most expensive marginal generator through this quirk of contract design, even if its unit costs are less than CfDs. For just 1.3% of 2025, electricity prices were lower than the weighted average CfD contracted (“strike”) price of £151 per megawatt-hour (MWh)[5].

% of 2025 when short-term wholesale prices (MIP) were higher than CfDs: just 4.1% for the future nuclear CfD and 1.3% for active CfDs

The good news is that contracted sites that have yet to be commissioned are much lower priced than historical CfDs. Future onshore wind (£58 per MWh) and offshore wind (£71 per MWh) prices were lower than gas over 73% of the time in 2025. Solar prices (£69 per MWh) beat gas 38% of the time, lower because it only dispatched during the day.

The bad news is that CfDs lock in prices at a time when costs could rise, for example due to supply chain shortages or grid connection scarcity. CfDs fix the price of electricity for fifteen, now up to twenty years, growing with inflation. Currently, CfDs account for around 12% of total electricity demand in the UK[6]. By 2031, they are estimated to cover 40%. This could go up even further depending on the outcome of future government procurement rounds. The government is also pursuing a significant nuclear strategy, which is unlikely to bring down energy bills by displacing gas based on the current nuclear CfD price of £127 per MWh.

Total electricity demand met by CfDs: 40% by 2031

These prices also exclude other costs like capacity markets, curtailment and balancing.

Capacity markets pay generators like gas plants to be available, even if they don’t dispatch. These payments are approximately £1.4 billion in 2025 calendar year, with annual costs rising over 50% from 2024/25 to 2025/26[7]. These payments subsidise wholesale costs. Spread across every unit of generated electricity in 2025, they reach almost £5 per MWh[8].

Curtailment is when generators are instructed to switch off because there is too little capacity on the network to deliver their electricity to where it is needed. This partly happens because Britain has not expanded its grid infrastructure sufficiently to connect its generating sites to its demand centres, and partly because the power market in the UK does not incorporate any constraints by location. At the time of writing this paragraph, Kilowatts IO estimated that over 1,700 MWh of production had been curtailed in the past 25 minutes. This alone represented £120,000 of payments to plants that switched off. If any of these sites had a CfD above the prevailing price of £71 per MWh, they would be paid even more.

Kilowatts.io real-time energy dashboard: watch and be mesmerised

Curtailment is considered part of balancing costs, which also include paying other generators to switch on in less constrained parts of the network to make sure demand can still be met from another source. There are other drivers of balancing costs like responding to outages, but energy imbalances from thermal constraints make up the lion’s share of the £2.5 billion cost in 2024, or £9 per MWh[8]. This cost is projected to be between £4.3 to £5.2 billion in the 2025 calendar year or another £15 to £18 per MWh.

NESO’s historic balancing costs and volumes: system constraints make up the majority of cost

The argument in favour of CfDs is that they lower the price of electricity through contractual certainty. Generators compete in the auction process for a contract rather than in the short-term markets. The CfD contract helps to lower prices because investors should be willing to accept a lower return on their investment if they are protected from price volatility and uncertainty. This protection also extends to their lenders, who may be willing to finance at higher loan-to-value ratios and lower rates. In theory, this reduces the price of renewable power because remunerating up-front capital expenditure is such a big portion of renewable unit costs. Bringing down the cost of financing, however, is no substitute for reducing the cost and speed to build or making the market more accurately reflect system constraints.

In 2025, there wasn’t a single half-hour period when gas didn’t supply at least one gigawatt of power. Reducing electricity prices is not as simple as building more renewables to use less gas if gas power is more competitive than CfD contracts. The government’s planning and grid reforms are a strong start. They need to make it cheaper and quicker to build energy projects in the first place, and reward plants based on what they physically deliver in a competitive market. Otherwise the government risks signing up to even more fixed capacity when it may not actually be any cheaper than alternatives.

As always I am open to feedback, but in particular welcome thoughts on extending this analysis or pushback on the approach. I plan to look at merchant capture rates for solar plants next, and an analysis on the investment returns of T&D companies. Hit reply or comment below.

[1] Honourable mention to “zonal pricing will create a postcode lottery” and “paying windfarms to switch off costs over £1 billion”

[2] Russia’s supply of gas to Europe started falling towards the end of 2021, which drove up prices before the Ukraine war began early the following year.

[3] Note how coal disappears as “solid fossil”. It sets the price ~20% of the time.

[4] 98% of the time is the figure sources often quote, but checking the original source it is 97%. It is unclear if the numbers in the study were revised, or just routinely misquoted across different platforms. In addition, Parliament references this as 2023 prices when this was the study publication year, not the year the data was collected.

[5] This calculation is a weighted average of LCCC’s strike prices across all the generation it paid for during 2025, including Investment Contracts and Allocation Rounds 1-5. Source data here. At time of download, data was current to December 18th with values imputed for the remaining days of the year.

[6] Depending on the denominator. I use NESO’s demand figure as it relates to grid power, which is slightly lower than the UK-wide total.

[7] The capacity market “year” is from October 1st to September 30th. I have estimated the 2025 calendar year figure by taking ~75% of 2024/25 and 25% of 2025/26. This is only an approximation as the estimate of the difference between years is 52% (£1.26b up to £1.92b) but this tracks with monthly capacity market forecasts rising in Q4 2025.

[8] Allocated just to the capacity market generators and when they deliver power, this cost is even higher.

This is a helpful summary, though as you point out, CFD's that are currently in operation reflect auction prices from some time ago. Like you I don't find the 'gas usually sets the price so lets get gas off the network' narrative terribly helpful. Even with some declines in pricing it is hard to justify renewables mainly on cost grounds; the rationale is about decarbonisation and, to a limited extent, reducing exposure to volatility.

It needs a braver government to explain the trade-offs.

Look forward to reading more from you.

"This cost is projected to be between £4.3 to £5.2 billion in the 2025 calendar year" -- where did £5.2 billion come from? The linked document shows a range of £2.5 to £4.3 billion.

"In 2025, there wasn’t a single half-hour period when gas didn’t supply at least one gigawatt of power. Reducing electricity prices is not as simple as building more renewables to use less gas if gas power is more competitive than CfD contracts" -- well both of those aged badly! OK the US and Israel attacking Iran was unexpected but gas gen falling below 1 GW was pretty much a given.

Might be worth updating the post.