Why Scotland wants a national electricity price and what it means for energy bills

Electricity markets are complicated, and going down the rabbit hole leads to terminology like ‘duck curves’ and ‘de-pancaking’. However, let’s indulge in some simplicity as we set up the latest UK debate over national and local electricity prices. For a moment, imagine you’re a humble Scottish apple salesman[i].

You have huge orchards producing tonnes of fruit nearby (perhaps even a few orchards on offshore islands?), but not nearly enough people to eat them up North. You want to ship it down to other parts of the country, like England, where there are more people who eat apples. The problem is, there aren’t enough trucks to get all the apples down to England in time, before they rot. As a result, would you expect the price of apples to be lower in Scotland than the rest of the UK, or higher?

An economist might say lower[ii]. Not many people live near your orchards who want to buy apples, so there is not much local demand. However, people in other areas would only want your apples if your local prices plus shipping are the same or lower than prices in England. If the route to market is constrained, an apple producer might even be willing to undercut prices to make sure their apples are loaded onto the truck bound for London. The trucking company pockets some of the upside for offering a sought-after delivery service. Refrigeration might also solve some of these options, by allowing you to store your apples until the trucks are less congested.

Yet if these apples were sold like electricity, they would trade for the same price all over the UK, no matter the constrained transport routes to get them to apple consumers. In electricity markets, the generator receives the same payment nation-wide for providing power in 30-minute windows based on an auction process. This is the same phenomenon that sees low-cost renewables receive the same price as higher cost gas at certain times of day. Meanwhile, the customer pays for the ‘transport’ charges of that electricity in a different part of their energy bill (network charges). Batteries can also provide a service akin to the apple refrigeration analogy by storing energy until the constraints are lower[iii].

These additional costs are not trivial: grid constraint charges (“balancing services”) have risen 9-fold in the past 12 years in Britain, from £220 million per year on average from 2010 to 2015 to ~£2 billion in 2022 according to an FTI report. Renewable projects are one of the drivers of the cost rise because of where they are sometimes sited: far from demand centres.

Herein lies the latest debate in UK energy markets: whether we would make the market more efficient and consumers better off by shifting to location-based prices.

The case for national

On the one hand, we have Scottish Renewables, a trade body, recently calling on the new UK government to rule out “locational marginal pricing” (LMP). A nationally-determined price likely benefits Scotland because of their significant low-cost renewables production and location away from demand centres.

In an analysis of a sample hour by FTI[iv], they found that a national price would see a close-to-zero marginal price for electricity, set by Scottish windfarms. Under a nodal market, prices might clear at £126 per megawatt-hour in the South of the UK, £3 per megawatt-hour in Northern England, and still close to zero in Scotland. Indeed, they “find that under a location pricing regime, wholesale electricity prices fall significantly in the northern regions of Great Britain.” Scotland would have some of the lowest wholesale prices in Europe in 2025, beating Spain, Norway and France, while the rest of the UK’s generators would command higher electricity prices.

Proponents of a single price (like Renewable UK) argue that it is simpler than a geographically-differentiated price (true), the switch would create uncertainty for project developers (also true as there would be no track record of pricing), and an increase in volatility would raise the financing costs for projects (also possibly true but perhaps balanced out by cheaper electricity prices overall in the more volatile locations). Some advocates also suggest that the price signals to develop projects won’t work if land development is restricted.

The most credible argument against locational pricing seems to be higher capital costs and risk for investors. Existing projects and those in construction were financed based on the existing market conditions. If investors receive less money for their existing projects, this might deter future investment and raise financing costs to better reflect their risks. This, in turn, would raise prices for customers. Aurora argue that introducing locational pricing could decrease consumer costs by 2.6% or increase them by 2.5% depending on the cost of capital of newly built capacity.

So why would a location-based pricing system be better?

The case for local

The UK’s Department for Energy Security and Net Zero compiled evidence from markets around the world to suggest that more granular pricing would benefit consumers without compromising energy security. One finding offers a clue about why energy groups, even progressive renewables organisations, might lobby against locational prices:

“Most of the benefits identified have been the transfer of congestion rents from generators to consumers”

The report also identifies efficiency savings in other jurisdictions:

“Generators incurred substantially lower operational costs through more efficient fuel use and ramping – c. 2.1% in CAISO [California’s electricity market] and 3.9% in ERCOT [Texas’s market]”

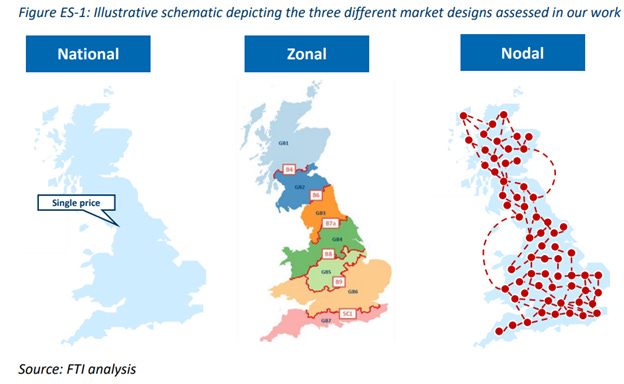

In 2023, FTI and Catapult examined zonal and nodal market designs for the UK and estimated consumer benefits of £15 billion up to £51 billion between 2025 and 2040. Zones would split the UK into seven districts reflecting the major electricity grid constraints (similar to Australia’s system), while the nodal approach modelled 850 different prices throughout the country (similar to American markets like Texas and California). The more granular market would be complex to implement but offers higher benefits because it more efficiently prices in grid constraints. If we get the transmission investments we need, FTI’s model still suggests a benefit, but 40-50% lower.

Critics of locational pricing suggest there would be a “post-code lottery” for electricity prices. However, differentiated prices may be desirable, for example as an incentive for electricity-hungry businesses like data centres to locate closer to renewable projects. This would have knock-on effects for economic development and potentially diversify Northern economies. Aversion to differentiated prices for households could also be resolved with a national average charge to end users while still paying the generators their geographic prices. This already implicitly happens with energy generation and network costs.

National price proponents also highlight that a locational price would not deliver its claimed benefits. Aurora’s report suggests that the price signals will have limited impact on building locations to achieve Net Zero by 2035. This is due to fixed factors like leases available for the seabed (relevant for offshore wind), the solar and wind resources at a particular site, the availability of cheap land, and permitting restrictions in built up areas. A high price signal for projects near demand centres like London is useless if projects can’t be built there.

Yet precisely the point of locational pricing is to account for the cost of constraints in the electricity grid, and the location of supply and demand in addition to all these other factors. If you had the cheapest and most productive wind site in a remote part of the country, this would not be a good deal for a British energy customer if the cost to dispatch it is excessively high. While planning may inhibit large projects near major cities, higher potential revenues could increase the uptake of distributed energy resources like solar panels, home batteries, and control of devices like electric vehicles to create “virtual power plants.”

Investors pay

While a locational system seems to provide more appropriate price signals for projects and where they should be located, investors experience many of the downsides. Under the modelling scenarios, power producers might expect to be between £9 to £27 billion worse off.

FTI’s report assesses what you would need to believe the increased risk to investors is that zeroes out the benefits for consumers. The financing cost increase that would eliminate all benefits is surprisingly low. Weighted Average Cost of Capital at an additional 139 basis points (bps) under an incremental policy scenario and up to 341 bps in the extreme transformation case would wipe out all consumer upside. For context, UK government bonds yields increased by over 200 basis points in the past two years. A further 100-200 bps rise due to uncertainty does not seem implausible.

UK 10 year Gilt Yields (%), last 10 years (FT)

Grid investment decisions are also out of an investor’s control, as the grid operators are separate companies. Along with all the other project variables, investors would need to form a view on the grid operator’s future grid expansion plans, and not just whether they can get a grid connection to their site. In Australia, which uses Zonal pricing, developers price in grid constraints via “Marginal Loss Factors” which reflect how far a site is from demand centres and the cost of dispatching its electricity throughout the day. This does influence site selection, but adds an additional layer of modelling complexity for the investor.

If you had to choose?

While I would like to see cheaper energy bills, I can understand why some investors wouldn’t want locational pricing here in the UK. I can also understand why Labour might be convinced to postpone locational pricing plans to show that they are on the side of investors.

Yet I think we would miss an opportunity to reduce energy bills by maintaining national electricity generation prices. The impact on generators could be reduced by sharing more of the efficiency benefits with them, or by offering more options to fix the price of electricity delivery to reduce their risk and financing costs. Location-based pricing could also offer incentives to move energy-intensive operations to parts of the country with cheap electricity, creating economic opportunities in those regions.

[i] I know the electricity market is far more complicated than this and am happy to chat with anyone about where this analogy breaks down

[ii] With caveats like whether the apples are more or less identical commodities, along with lots of other conditions economists like to impose like many sellers and buyers, information transparency, etc. etc.

[iii] Though in this analogy, apples could probably be stored for days or weeks whereas most UK batteries can store just a few hours’ worth of energy.

[iv] Page 14/15