This Week's Energy: undervalued coal privatisations, off-grid data centres, collapsing power prices and more

What caught my eye in the news this week

This week I am trialling a newsletter-style post rather than my usual long-form analysis/op-eds. Expect a long-form on Monday.

These are drawn from this week’s LinkedIn posts - follow for updates, and read on for the highlights. Drop a comment on what catches your eye!

This Week’s Energy

Getting more bang for buck on rooftop solar in the Warm Homes Plan

How EVs can help when power goes down, like the storm in Cornwall

Should data centres go flexible and off-grid? In the US, 33% plan to.

Indian government partially privatises coal mine, but at the right price?

Australia’s Q4 2025 power prices halve after renewables boom

How UK cuts to renewables subsidies could change investment sentiment

How Amazon lay-offs could impact the UK former coalfields

Transmission costs are putting off UK wind developers

China tripled oil & gas BRI engagement abroad in 2025, mostly in Africa

Offshore wind is about security not cost reduction - Hamburg & CfDs

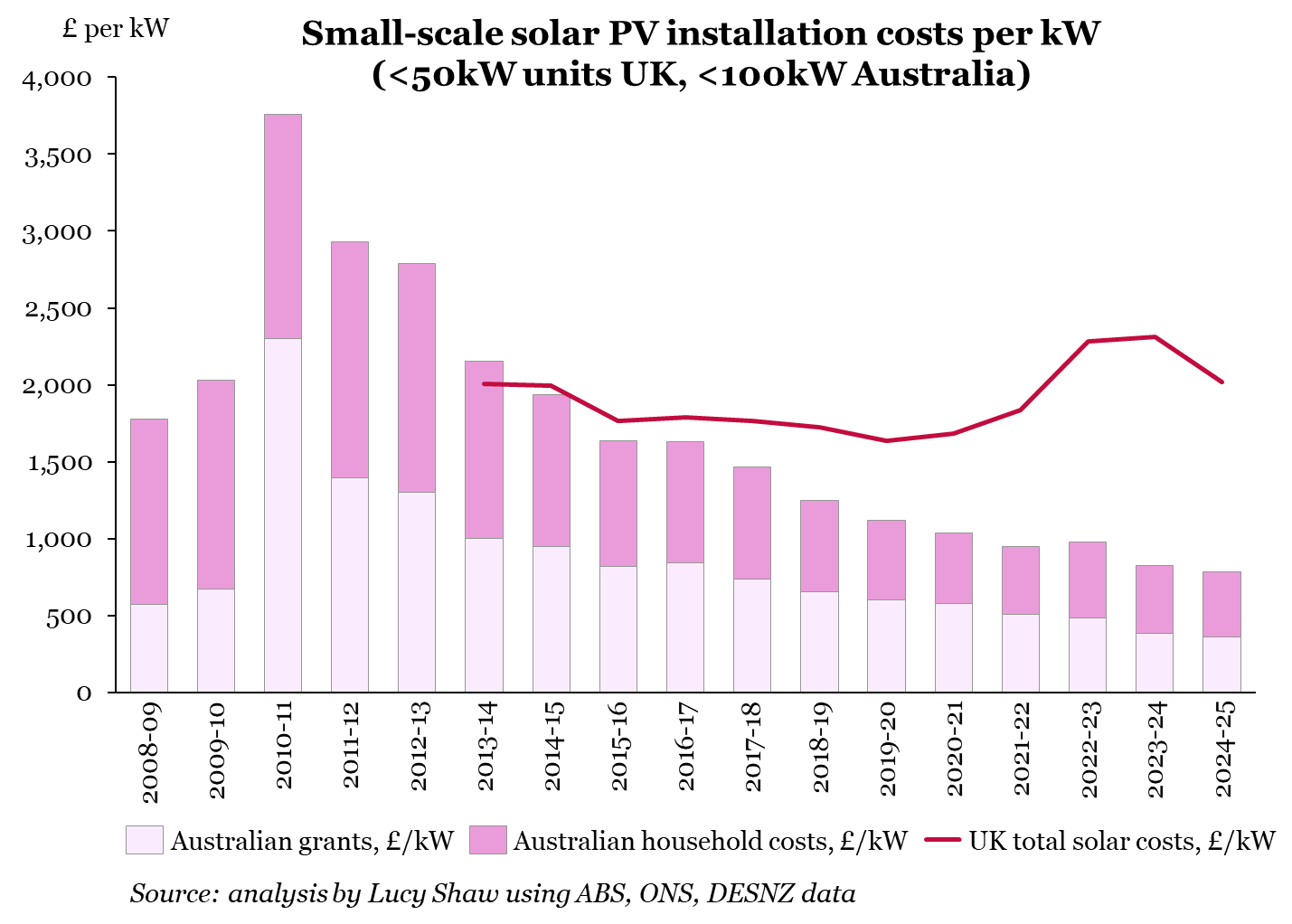

Getting more bang for buck on rooftop solar

UK rooftop solar costs 2.6x more to install than in Australia. The Warm Homes Plan's £15b investment is welcome, but the government should get more value for money.

The Warm Homes Plan will fund upgrades to reduce energy bills, mainly in heating but also in electricity investments like solar and batteries.

The input costs of solar systems have plummeted, but British installation costs haven't. The government could get more value for money, reach more homes, and save more on bills by helping to bring down unit installation costs.

How could it do this? Some ideas from Australia and beyond:

Reward speed: installers who deliver fast have less customer attrition and lower customer acquisition costs

Coordinate installations: reduce fixed costs of scaffolding, planning applications, and disruption by joining forces with neighbours

Public procurement: generate scale benefits from higher volumes via councils, social landlords, and large scale customers (similar to GB Energy's NHS and schools deal)

Aggregated procurement: support installers to get better deals through a central facility, similar to programs for the off-grid solar sector in Africa

Streamline planning applications and safety / quality inspections

Automate the approval for any required grid upgrades and deliver these on time

What do you think - are the high costs of solar justified in the UK, and if not, what could reduce them?

How EVs can help when power goes down

When I visited West Virginia, tens of thousands of residents were cut off from power. Reliable coal couldn't help them when storms brought down powerlines. More Electric Vehicles might have.

Even a portion of an EV's charge can power a household for days. This means people could still drive if they used EV charge to power their home. They also have the choice between driving and electricity, an option petrol cars don't offer.

Really interesting to see reports in Cornwall of people using their EVs to deal with power outages due to weather.

I think demand response and in-home energy storage is a still untapped opportunity and could go a long way towards reduces energy costs and increasing system resiliency. Not everyone in the UK can or should own a car, so other solutions like batteries can help fill that gap.

What do you think - should we be supporting EVs more as a grid resiliency measure, not just for carbon emissions, air quality and fuel cost savings?

Should data centres go flexible and off-grid?

Energy for AI is constrained. This leads to extremes like delaying coal retirements, or using jet-engine-like turbines to get projects powered up before the grid arrives. According to Cleanview, 33% of data centres in the pipeline are planning to be off-grid in the US.

The largest models need always-on power and fast. They could checkpoint to tolerate downtime and intermittency, but time is the ultimate commodity. It's a race to develop the next model ahead of competitors. Intermittent power may be cheaper, but reduces utilisation.

Nimble providers can innovate by offering flexible data centres, building modular generation systems and making use of cheap energy for customers that can handle shut-downs in their workflow.

They may not attract the largest model developers but they serve a flexible customer segment that otherwise would be squeezed out from the data centre capacity landgrab.

What do you think about the potential for modular data centres to deliver compute for AI developers?

This discussion was part of a panel at SALT London on AI infrastructure and applications, building on my column on the same topic last year. Watch the full panel here.

Did India get a bad deal on its coking coal partial privatisation?

When governments privatise assets, setting the price is lose-lose. Sell too low and citizens lose out. Sell too high and no one will buy it. How do we rate the Indian government's $119m coal privatisation this month?

India's coal mines are predominantly state-owned, and the largest coal conglomerate is Coal India. Earlier this month, they sold a ~10% stake in their subsidiary, Bharat Coking Coal, via an IPO. I visited one of BCCL's underground mines on my last trip to India.

The IPO was way over-subscribed, and the stocks priced at the top of the issuing range, ₹23 per share. This generated $119m (before fees) for the government, and ultimately the people of India.

When the stock later listed on the market, it 'popped' to ₹45 per share, a 96% bump. This enthusiasm for the stock is potentially $114m of value the government left on the table.

Since the debut, the stock price has fallen to ~₹38 per share, still a 65% premium to issue price.

So was this a good deal for India, or for the investors?

Companies may want an IPO to pop above issuance price to generate buzz, and attract demand for future stock issuances. But they don't want it to pop too much otherwise they lose potential money they could have raised.

Governments face a similar problem, but they're accountable to citizens for getting a good deal.

Coal for steel-making is harder to displace than coal in the power sector. Coking coal is a more valuable and resilient asset than India's lower quality coal resources. Even if coal quickly exits the power sector (I don't think this is at all likely), coking coal has much more time to turn a profit.

India also doesn't price in all the externalities of coal, like health or environmental costs, and it doesn't invest coal profits in a fund to support people when coal eventually goes away.

My view is that selling one of the best state coal assets with this many subsidised externalities should probably have generated more value for the Indian taxpayer than its issue price, even with the decline since its stock listing.

I'm curious what you think about how government gets the most value out of privatising state assets and any examples of this going really well or really terribly?

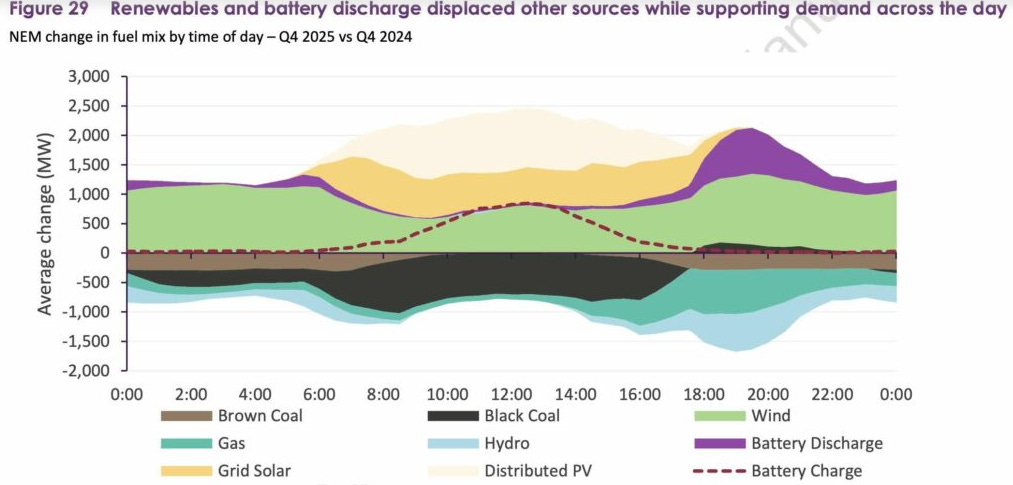

Australia’s Q4 2025 power prices halve after renewables boom

A headline the UK would love to have - '“Landmark moment:” Prices plunge as renewables supply half of grid, batteries surge and [fossil fuel] hits new low.' Alas, this is Australia, where wholesale prices fell 50% to ~£25/MWh in Q4 2025.

The chart shows how the mix of different technologies changed between Q4 2024 and Q4 2025 for average dispatch across the day. Wind, solar, batteries are up, while coal and gas are down (also hydro, not sure why).

"As usual, average wholesale prices were lowest in those with the biggest share of wind and solar – such as Victoria and South Australia (both ~£18/MWh) – and highest in those most dependent on coal, NSW (~£37/MWh) and Queensland (~£29/MWh)."

This is an incredible result that the UK could only dream of. That would be a >2/3rds drop from UK 2025 average prices, and is less than half of our cheapest CfDs.

It may not last. "The March quarter is likely to tell a different story given the extraordinary heatwaves that swept the country in January."

It also may not impact total bills much, or soon. From The Guardian - "Network costs make up about 39% [of bills], while 16% goes to energy retailers’ administrative costs and profit margin. About 7% covers environmental policies." "The falls in wholesale prices ... may take time to flow through to customers because energy retailers often sign contracts for electricity years in advance."

I'm especially interested in how market design and mix of contracted vs wholesale power can drive a similar outcome for the UK. What do you think the UK could learn from the Australian experience?

Read more from Giles Parkinson @ at Renew Economy

And Petra Stock @ The Guardian

UK cuts RO subsidies by changing inflation linkage

30% of the UK's electricity is subsidised* and rises with the 'retail price index'. By switching to CPI, the government saves ~90-120 bps of annual price increases**. Should investors be upset?

Companies underwrote energy projects assuming an RPI forecast, not CPI. Because of its methodology, RPI was consistently above CPI - ~90 bps over the last ~40 years and ~70 bps higher when ROs were first introduced.

Investors would have factored this into their returns calculations, and believed the government would honour their contracts.

The government at the time was trying to incentivise renewable development, and inflation linkages helped. It doesn't exactly reflect the ongoing cost inflation of running a renewable project, as the bulk of expenses are upfront.

In my view, UK investors have done very well out of the RO scheme, especially with above average inflation long after many projects were in the ground, and the falling cost of financing since ROs were introduced. I don't see it as a big issue to bring cost rises in line with inflation, and indeed can even see a case for keeping them fixed in nominal terms or shortening their duration.

Nonetheless, I expect investors to be grumpy about this change, and claim that it increases the cost of capital of investing in UK energy because the government can't be trusted to stick to their contracts. But the decision to share some of these gains with consumers on affordability grounds feels like a small price for investors to pay. Opposition parties have pledged to scrap carbon pricing and subsidy systems entirely if they get into power, and this appears to be resonating with a large number of voters.

What do you think about this RPI change? Is the £270m annual gain worth any potential 'investor confidence' hit?

*You could argue more is covered under CfDs, also indexed to inflation, but this is not a straight subsidy as it is structured as a price guarantee - it's just turned out as subsidies way because contracted prices have usually been higher than market prices.

** Average of last 10 years is higher, ~120 bps.

Former UK coalfields are more exposed to Amazon lay-off risks

You know which British regions are highly dependent on warehousing jobs? Former coal communities. Will Amazon's mass lay-offs be the new miner's strikes?

From the Coalfields Regeneration Trust in 2024:

"Across the former coalfields, warehousing employment is now beginning to match the number of jobs in the coal industry itself in the years prior to the 1984/5 miners strike." 176,000 jobs in total as of 2022, often on the site of former coalmines.

"The warehousing jobs are concentrated. There are almost 60,000 in the former Yorkshire coalfield. The adjoining coalfields in Nottinghamshire and North Derbyshire account for nearly 30,000, and there are 20,000 more just across the Pennines in the former Lancashire coalfield."

Keep watching these updates to see how many of these job cuts will be in the UK - and where. The impact could be devastating if these jobs are concentrated in regional areas that already face worse health and employment outcomes than the UK average.

Balancing resource availability and transmission cost is hitting investment

Building projects where it's windiest isn't enough to make them the cheapest - the power needs to get to where people use it.

Wind developers in Scotland are being hit with higher transmission costs than those sited closer to demand centres.

This seems like a good thing to me, because it recognises the system costs of electricity, not just its unit costs. It incentivises projects to be built where the all-in cost is lowest.

As a counter example - the UK has low solar irradiation compared to other booming solar markets, and middling to high solar build costs. But solar is still cost-effective here versus alternative technologies.

We accept that the cost of upstream transport is embedded in the fuel price for resources like coal and gas. Although transmission costs are a different concept, it seems odd to consider resource availability of renewables but ignore "transport" costs at dispatch when choosing where to build new projects.

I do think there's a case for subsidising T&D for rural electrification - but that's a different issue from subsidising rural generation to connect to demand centres in cities.

China tripled oil & gas deals abroad in 2025

In 2025, China's BRI engagement in oil & gas almost tripled to $71b. This dwarfs clean energy investments at $18b. For an 'electro-state', they seem quite keen on fossil fuels....

Dr. Christoph NEDOPIL WANG's new report on BRI from Griffith University has a lot to unpack. Here's what stands out to me:

🌍 Africa received ~48% of construction contracts and ~22% of investment for a total of $80b in 'engagement' (out of $214b globally).

⚡ Energy engagement was the largest category at $94b, and more than doubled from 2024.

🔥 Fossil fuels were 76% of energy engagement - and this share rose since previous years.

⛏️ China is still investing in coal-related assets abroad ($2.5b), primarily mining infrastructure.

👷 'Exploitation' (mining, oil & gas extraction) was more than half of energy engagement.

🛢️ All the figures above are heavily skewed by two investments (46% of energy; 54% of Africa): $23b oil and gas project in Republic of Congo and $20b gas development in Nigeria.

What do I think?

The electro-state narrative is right in that China is building more renewables than anyone and supplying the world, but they are still very much in the market for fossil fuels too. Adding more renewables does not reduce emissions unless fossil fuel consumption goes down.

BRI funding for renewables looks strikingly low given China's huge clean energy manufacturing sector, but China may not need to push its products with BRI funding to drive exports given their competitive price point.

Investing in oil and gas is helpful given China's more limited domestic production of these fuels. They don't need to supplement coal so much.

BRI engagements don't read like aid or plunder, but projects with commercial and industrial benefits for both parties.

Single year figures are lumpy - mega projects skew the results - so watch for sustained trends over time.

What jumps out at you from Christoph's report?

Offshore wind is about security, not cost reduction

Gas prices are up >30% in January - a reminder of the price shocks and energy dependency that renewables protect against. This week's Hamburg declaration on offshore wind is framed as a 'security pact', unlike 'bill-cutting' CfDs.

The Hamburg declaration, a collaboration on 100GW of offshore wind development in the North Sea, greatly emphasises security in its press release. This feels right to me, as offshore wind isn’t always the lowest cost.

The typical pro-renewable narrative on the UK’s CfDs is that even if they price at levels above today’s wholesale rates, they reduce cost by two primary mechanisms:

1) Displacing gas to reduce traded wholesale prices

2) Avoiding investment in even costlier technologies

To be clear, I am also pro-renewables and pro-climate action. But when a voter thinks about the promise to cut energy bills, it isn’t about whether the government avoids higher future costs - it’s about whether their bills are actually lower than last year.

As the UK Energy Research Centre (UKERC) reported this week, 2/3rds of the price rise from 2021 to 2025 was from an increase in gas prices. I have a hard time imagining how a unit CfD price that is 17% higher than 2025 wholesale prices (set by gas) and linked to ongoing inflation will lead to bills going down in absolute terms when those projects come online.

These CfDs could reduce traded prices for gas on wholesale markets - but then customers are hit with a subsidy top-up.

This linkage does have a positive outsized impact because CfDs are a small share of total demand. But when CfDs start to represent 40%+ of the market (the estimate for projects through to AR6 as a share of energy demand in 2030), they need to deliver a larger saving across a smaller amount of generators remaining on wholesale markets. And if wholesale generator costs do plummet, it will beg the question of why so many generators are locked into higher priced contracts.

I’m also speaking in terms of comparing energy costs to prior years. Estimates I’ve seen of savings from CfDs are often avoided costs rather than actual cost reduction. Avoiding cost is great, but I can understand why people get frustrated when they are told bills have been brought down by renewables, then see prices go up - as they did this quarter.

I see the government prioritising energy security and protection against price shocks with their offshore wind CfDs and the Hamburg declaration, which is a really important goal.

But I think we need more discussion among the pro-renewables crowd on whether policies are about cost management or deliver other important benefits, and how we communicate this to voters.

Other policies will bring costs down, so why does offshore wind need to be sold on cost instead of security? We risk disappointment and even more net zero backlash if we get the message wrong.

Read more in my LabourList piece last week.

If you like these emails, subscribe to receive regular long-form analysis and send them to your colleagues and friends, and follow me on LinkedIn for regular timely updates.

Absolutley brilliant roundup. That Australia power price drop to £25/MWh really highlights how renewables deployment timing matters. The 39% network cost staying flat even as wholesale collapses is crucial tho. We ran into similar situations where transmision bottlenecks ate the savings from new storage. Those regional gaps (Victoria/SA at £18 vs NSW at £37) kinda show coal areas lag behind on the transition benefits.

It’s interesting how often what’s labeled ‘undervalued’ isn’t just about numbers, it’s about narrative. Do you think coal’s story is being rewritten… or simply re-priced?