Coal's second life: how to turn liabilities into infrastructure for the future

Looking out on the brooding waters of the Bristol Channel, I couldn’t help but think that this would make a great destination for a writer’s retreat. Alas, the Cardiff Capital Region has other plans for the site of the former Aberthaw Coal Power Plant.

With 500 acres of land, a former grid connection of over 1.5 gigawatts, and proximity to local ports, this site is an infrastructure developer’s dream. Making it a reality faster will require a recognition of former industrial sites as strategic national assets. Governments need more accountability to create value from these sites, and more national-level support for local officials to develop their vision and execute it.

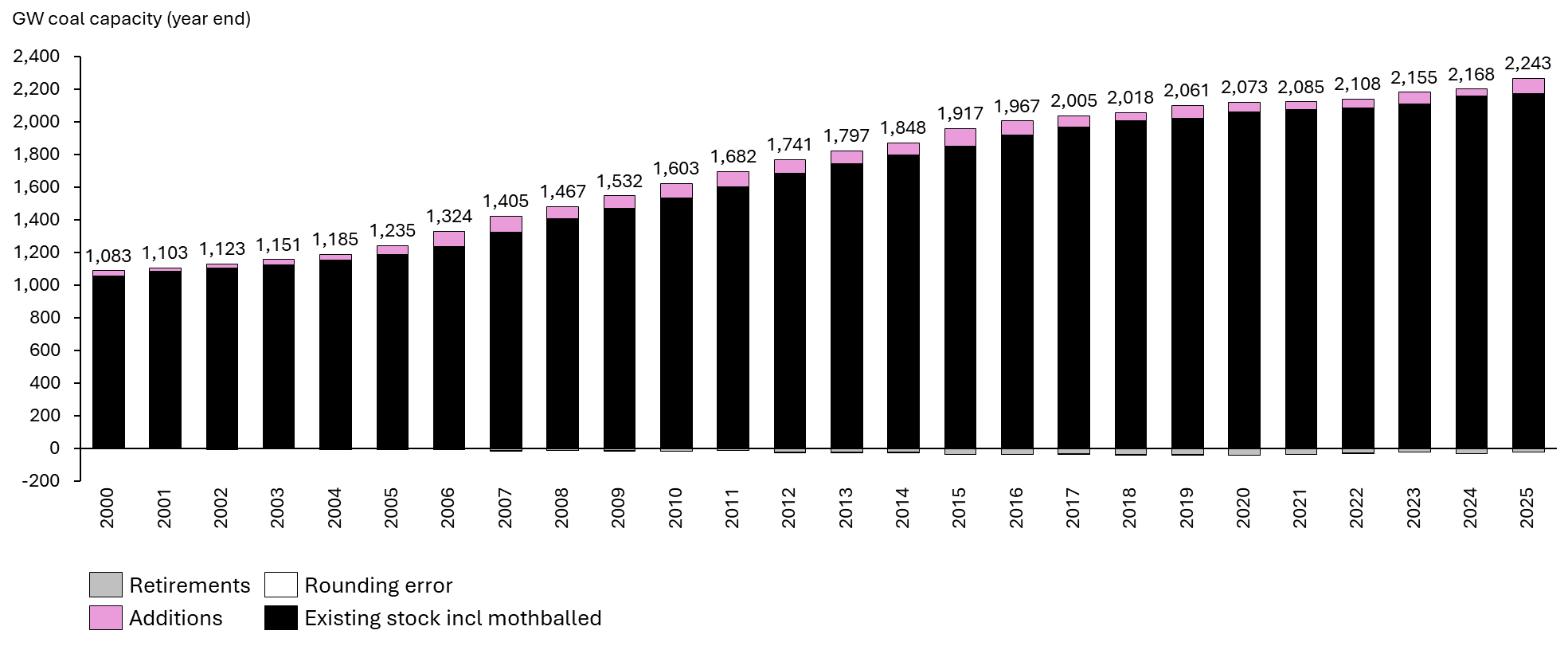

Solar and wind get so much attention for disrupting our landscapes while most people never see the scale behind the coal power industry[i]. Around the world, there are 2,200 gigawatts of operating coal power plants, 8.9 billion tonnes per year of coal mine capacity, 369 coal terminals with a capacity of 6 billion tonnes, and thousands of kilometres of rail networks[ii].

While coal is gone in the UK, it still produces over a third of the world’s electricity. In absolute terms, consumption reached a new peak in 2025. If renewable energy, storage, and flexible power accelerate the decline of coal[iii], there is a staggering amount of infrastructure to decommission. That’s before considering 20 terminals, 296 mines, and over 240 gigawatts of generation capacity currently under construction, and more potentially in the pipeline. Instead of letting this industrial infrastructure go to waste, giving more thought to coal assets’ second life before it closes would help to defray the cost of early retirements and remediation liabilities.

Retiring coal assets is not a new problem. The industry has been decommissioning sites for hundreds of years. Mines run out of resources that are profitable to extract[iv], and coal power plants are built to last for decades, not forever. Over 500 gigawatts of coal capacity has been retired since the year 2000, of which 60% was in the US and China, two of the world’s largest coal consuming countries in 2025[v]. Almost 1,500 mines were closed between 2015 to 2024 alone, 80% of which were in the US.

Installed capacity of coal power globally by year, net of annual additions and retirements

The scale of the retirement challenge has grown, but what’s new is the scarcity value of what these sites can be used for instead. Data centres, decarbonisation, electrification, and re-building a manufacturing base closer to home are all driving up demand for land and grid connections. Former coal sites could meet the moment, if they were seen as an asset to be monetised rather than a remediation liability.

Data centres are a particularly hot opportunity for former coal power plants, as the AI boom has developers in a frenzy to search for grid access, industrially zoned land, and access to water for cooling. Again, this conversion trend is not necessarily new. Google announced a coal power plant redevelopment into a data centre over ten years ago in the US, but the idea has taken time to spread. In the UK, Blackstone is developing a gigawatt-scale data centre campus on Blyth power station’s former coal stocking yard[vi], while Start Campus, backed by Davison Kempner and Pioneer Point is building at a former coal plant by the sea in Portugal. Keppel announced just last month that it would invest A$10 billion in a data centre in the Latrobe Valley, home to Victoria’s brown coal industry in Australia.

British coal power plants have also been converted into gas or biomass facilities like Drax, or demolished and used for batteries, solar generation, homes, and even Amazon warehousing[vii]. The US and China have developed gigawatts of renewables on former mining land in addition to remediated forests and tourist resorts[viii]. In the UK, mining land is occasionally redeveloped into real estate, which benefits from adjacent transport links and labour. Water within abandoned mines is now being used for heating homes in Gateshead, England. Some power stations are even aesthetically pleasing enough to be used as museums, like the Tate Modern in London, or shopping and housing precincts like Battersea Power Station.

These successes are striking because they are often the exception rather than the rule. They are fragmented projects driven by local authorities, existing owners and new investors. There are few if any national strategic plans for repurposing coal assets[ix] and projects can languish for years with no progress or support, and there is a long tail of projects with no redevelopment plan at all. Private owners may stall development plans or a sale if the investment options aren’t clear. Local governments may only deal with one or two remediation sites in their area and sometimes lack support on how to structure, select, and progress the best deal for their constituents.

For example, Blyth’s redevelopment into a data centre was far from inevitable. The coal plant was closed in 2001 and demolished in 2003. Its private owner kept the property and explored the option of opening a new coal power plant on the same site before abandoning the idea. A wind turbine factory was floated as n option, before the site was finally selected by Britishvolt as the home of a new battery factory – 17 years after it was demolished. This project was eventually cancelled when Britishvolt went into administration, and Blackstone signed up to take over the site in 2024 to build a data centre, which is still under construction.

If there had been national support to develop a plan for the site when it first closed, the local government could have offered partnered with the owner to convert it to housing, industrial facilities, a factory, or renewable generation and offered mutually beneficial incentives. While the multi-decade delay to develop the site has led to using it for a high-value data centre development, the land could have been put to better use of the past 25 years.

Around 25 major coal plants were retired in the UK since 2000, and less than half have completed their redevelopments with some still lacking any concrete plans at all. For example, the Rugeley Power Station conversion into over 2,000 homes was announced in 2018 but only received planning permission in 2025. Renewable projects on former mining land like Fife’s 80 megawatt solar development in Scotland are a rarity, and even this one remains to be built. Remediation and sourcing the best investment opportunities do take time, but other places have been able to deliver faster. Myriad solutions have been tried and tested in patchwork programs around the world. Our governments could be learning these global lessons to support their regional authorities to think strategically about how to monetise valuable industrial assets for the modern era.

What would that support look like?

In the UK’s case, where all the assets have already shut down, the national government could work with regional counterparts and international experts to collect the best practices for redeveloping these sites and an inventory of opportunities for investors. The Department for Energy Security and Net Zero, the National Wealth Fund, and Great British Energy could develop a guide for how to prepare a site for its second life and support local governments to structure negotiations with the private sector to create the most value from their industrial assets. Developers could in turn be encouraged to review coal re-developments more closely, for example drawing more on the Mining Remediation Authority’s structural surveys to identify sites where it is safe to build generation assets and logistics depots.

Deal support for local governments could include benchmarks for the typical rents that renewable firms, data centres, and real estate tenants pay so that councils can weigh the trade-offs of different use cases against other benefits like job creation. Education on the breadth of commercialisation opportunities available, from an outright asset sale, to lease agreements and profit shares, could also help regional authorities negotiate the best financial outcome for their risk tolerance. The national government could pre-qualify developers so that individual councils are not duplicating efforts to assess their quality. The government could also support on financing and de-risking projects, offering bridge funding, guarantees and even equity and debt investments to get redevelopments off the ground and build traction with private developers.

In countries where coal assets are yet to be decommissioned, businesses and governments alike should start thinking about how best to monetise their assets once they are no longer needed. This includes designing mine and power plant closures to be able to capture critical minerals from waste, maintaining grid infrastructure so that it can be repurposed for a new site, and planning remediation so that the land can be used for solar and battery technologies. China already does this at scale with its abandoned mine lands. A systems approach, advocated by Duke University, could also unlock opportunities that bilateral deals for single sites might miss. These investments can help to maintain economic activity in communities that have seen coal jobs decline and reduce the net liability of remediation by creating value from an otherwise abandoned site. Even if they don’t create long-term jobs, they can offer infrastructure that underpins the modern economy.

A group of intrigued infrastructure investors visited Aberthaw in the summer of 2025 to discuss what could be done with the site, and they were brimming with ideas. There is a growing appetite from the private sector to understand the opportunities that industrial revitalisation offers. The national government could unlock investment and jobs growth if it offered strategic support and a deal playbook to the regional governments tasked with their redevelopment, and keep them on track to deliver results. This could help places like Aberthaw to revitalise in years, not decades, and build valuable infrastructure that the UK sorely needs for growth.

Subscribe for more updates on the energy transition, and share my piece with anyone you think should read it. Drop a comment with your thoughts on how we can use industrial assets for the infrastructure of the future.

[i] More on land use for different electricity sources at Our World in Data.

[ii] Global Energy Monitor is an excellent resource for energy assets.

[iii] CREA reported that China and India coal consumption for electricity went down in 2025 in a landmark moment, though they also point out that China keeps expanding its coal sector. Ember reports frequently on the rise of renewables and fall in coal in Europe.

[iv] Profitable to extract is an important distinction from running out of resources generally. The UK sits on hundreds of billions of tonnes of coal deposits, which are primarily deemed uneconomic to extract.

[v] China was the second largest coal consumer, the US was the third largest, in 2025. Although it is the third largest consumer, China consumes more than half of the world’s coal and the US’s coal consumption is less than 10% of China’s per year. Coal 2025, IEA.

[vi] Full disclosure, I used to work at Blackstone.

[vii] The article talks about how much Amazon warehouse jobs are much less inspiring than former coal jobs. I see this as part of the decline in pride and culture in coal communities, even if there is still technically employment - more on this, check out my piece in LabourList.

[viii] For example, Chief Logan State Park in West Virginia.

[ix] See Duke University’s new paper for an exploration on the approach of the US, India, and South Africa

I looked up Battersea Power Station and Tate Modern. The former was idling for 30 years before refurb started in 2013. Tate Modern was dormant for nearly 20 years.

Prime infra collecting dust instead of creating value for decades - really reinforces your suggestion that there’s room for more national level decisiveness given what we can do with these sites

All the coal stn sites should be restricted to energy assets only as those grid connections are gold dust and absolutely key to decarbonisation. CCGTs with CCUS retrofit should have first call followed by BESS assets next. SMRs if they ever get off the ground would also be ideal candidates as well.