Cheap solar and batteries still can’t match India’s $11b+ coal rents

Renewables will need to compete on upstream benefits like tax revenue, foreign exchange savings, and energy independence to push coal out of the system faster.

As the last shard of light escaped under the elevator door, I asked Sumit how deep we were going. 538 metres, he said. I felt woozy. I had never been so conscious that the oxygen in the air could vanish. I followed his instructions to take deep breaths and relax. After a clanking eternity, the lift finally reached the working level of the Moonidih mine in Dhanbad, India’s coal capital. We were greeted by a throng of workers waiting to return to the surface at the end of their shift.

Since the Moonidih mine in Dhanbad was built in the 1960s, India’s coal consumption has grown 15-fold[i]. As of 2025, India’s coal production was the second highest in the world at 1.1 billion tonnes per year, dwarfed only by China. India is still expanding its coal mines and power plants, even as solar and batteries now rival coal to deliver low-cost and reliable electricity.

At the power system level, it makes economic sense to stop using coal when it becomes more expensive than alternatives. This is already happening in market-exposed energy systems, and India saw a 3% decline in coal power consumption in 2025. Long lead-times to install plants, increasingly cost-competitive clean energy that can deliver reliable electricity, and the steep environmental and health costs of coal are all trends that should suppress demand.

To understand why coal power persists, look for the benefits upstream. Coal-fired electricity is usually provided by a domestic mining industry, with just 16% of global coal production crossing international borders[ii]. Coal mining offers advantages like employment, tax revenue, currency management, and international independence. This is before considering the opportunities coal creates for political donations, fighting culture wars, and even corruption. Renewables, nuclear, or gas may deliver cheaper electricity but may struggle to replace the macro benefits of coal, especially if governments continue to avoid pricing in health and climate impacts.

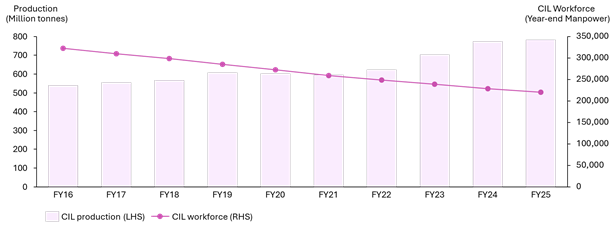

For India, coal jobs are important, but not the whole story. Despite announcements of recruitment drives and job creation, workers are also retiring or being pushed out by machines. This was confirmed by staff at Moonidih, a subsidiary of the largest government-owned coal company, Coal India Limited (CIL). CIL employed 220,000 people as of 2025, 32% fewer than in 2016. Over the same period, production increased by 45%, more than doubling productivity per worker. Pressure to reduce costs has led to more outsourcing and less stable employment, with CIL now indirectly employing 114,000 contractors in 2025.

CIL production and workforce, FY16 to FY25

Even with adjacent jobs, possibly as high as four million in 2021, the Indian coal industry employs less than 1% of the working population. Renewables already employ over one million people in India, and the sector is rapidly growing. However, coal is regionally concentrated, which leaves some locations exceptionally exposed to job losses. NGOs have been calling on the government to support workers losing their jobs as coalfields become more efficient or decline.

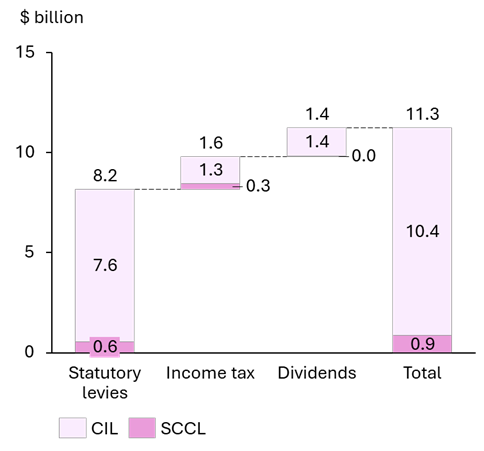

The real prize of coal seems to be government revenue. The government controls 85% of the country’s coal production via two companies, CIL and SCCL[iii]. In 2024/25, the Indian government collected over $11.3 billion in revenue from royalties, dividends, and income taxes from these two entities[iv]. Locally mined coal generated over $8 billion in levies for state and national governments, $1.6 billion in income tax, and $1.3 billion in dividends from state-owned coal profits. The government’s 74% stake in CIL[v] is worth over $20 billion at current market prices, and the government periodically sells shares to raise additional revenue.

Estimated government revenue from state-owned mining entities CIL and SCCL, 2024/25

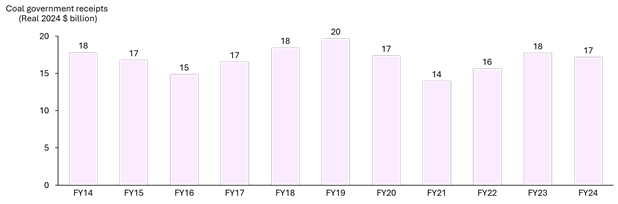

These two entities alone generated the equivalent of 1.4% of India’s national and state government revenue in 2024-25[vi]. IISD estimated that the government’s coal revenue across all sources was $17 billion for 2023/24, or 2.3% of the total[vii]. This might sound small but remember the drama around Britain’s budget “black hole” in 2024. This £22 billion shortfall represented 1.9% of all government receipts[viii].

Estimated total government revenue from coal, FY14 to FY24, Real 2024 $ billion

Coal also offers other macroeconomic upsides. Growth in domestic coal saved $5.4 billion in foreign currency for imports in 2023-24, a meaningful boost to the current account deficit of $23.3 billion. Continuing to use coal reduces dependence on importing foreign products, including solar panels and batteries from China. Coal also subsidises India’s railways, with freight payments amounting to $10 billion in 2022-23, around 33% of the railway company’s total earnings.

Keeping coal in India’s energy system is an indirect way to collect extra tax revenue via electricity bills and subsidise other services. This is not so different from the UK levying a carbon tax on electricity generators through energy bills and using the proceeds to fund billions of pounds of general government spending. This is in stark contrast to India’s approach for state-owned railway operations, which operate with almost no profit margins to offer low-cost passenger services.

These coal rents mean government has some leeway to protect coal in the face of competition from renewables, by removing coal taxes or reducing state-owned enterprise dividends. The government already cedes at least $3.2 billion in revenue from discounted import tariffs and sales to utilities. It reduced coal costs further in September 2025, by replacing a coal tax (‘compensation cess’) with an increase in GST.

Renewables will need to offer more than cheap and reliable electricity to displace coal at a faster pace. Clean energy already provides large-scale employment but domestic company profits have yet to generate the same rents that coal provides the state. Solar and battery installations have been historically dependent on imports, with a significant portion sourced from China despite tensions between the two countries. The Indian government and cleantech industry recognise this, with a push for domestic manufacturing to generate local income, maintain independence, and manage foreign exchange. True independence will require more than just local assembly and component manufacturing, but also sourcing and processing raw materials domestically.

Pushing the government to recognise the environmental and health damage of coal in energy bills would help even more. In Dhanbad, the hills are literally on fire and have been for over a century. Homes spontaneously combust and residents inhale polluted air. Across India, millions of people die prematurely due to fossil fuel particulate inhalation each year, yet the government recently exempted 78% of coal plants from installing equipment that would protect against harmful pollutants. The government’s coal taxes could be considered compensation for these effects, but this revenue is not set according to coal’s health and environmental damage, nor is it necessarily spent on remediating these issues. The renewables industry could lobby for coal taxes to reflect these costs, and for proceeds to be invested in transition funds instead of in-year general spending.

As the world’s third largest carbon emitter, India’s coal future matters for global climate change, and it also impacts human health. Accelerating clean energy installations in India is not just about matching coal costs and reliability at the power plant level but delivering comparable benefits to the state like tax revenue, independence, and foreign exchange savings. It’s too soon to celebrate last year’s decline in coal consumption. Until clean energy can match coal’s upstream pay-offs, or coal’s true costs are reflected on energy bills, coal is likely to remain in the system longer than power plant economics alone would suggest.

Subscribe for more updates and analysis on the energy transition. I focus on the UK energy sector and the global coal transition, but occasionally publish on other topics.

[i] Measured in Exajoules, not tonnes, due to data availability.

[ii] IEA Coal 2025, tonnes traded (1.5 billion) divided by tonnes produced (9.1 billion).

[iii] Singareni Collieries Company Limited, jointly owned by the Telangana state government (51%) and national government (49%).

[iv] This is my estimate for CIL and SCCL. I have not included benefits/dividends from the power companies like NTPC.

[v] Direct stake of 63.1% and indirect stake of 10.8%, a 11.2% stake held by a 96.5% state-owned life insurance agency

[vi] Using national revenue of ~$365 billion, state’s own revenue of ~$309 billion, shareable transfers of ~$153 billion. This method is line with the totals used in the IISD report for prior years, rolled forward to 2024/25.

[vii] IISD’s estimates includes CIL and SCCL, as well as revenue collected from customs duties and GST outside of these two entities. Detailed excel files here.

[viii] Using financial year receipts from April 2024 to March 2025

it's all a bit like the UK and Norway and North Sea oil revenues really, except that it's India and coal!

If you strip out all taxes and government charges (as well as interest income) from the Coal India accounts it is extremely profitable. In sterling terms, just over £6bn profit before government levies on just under £15bn of sales - a 42% margin, so there is scope for a lot of reduction in price if there is a desire to compete with solar.

Though I dont know at all what taxes solar has to pay in India, or what its margins are.